By Saxon East

Eamonn Flanagan was a seasoned analyst with a bearish attitude to UK motor insurers, and on this particular day, esure was in his sights.

Slapping a sell on esure, Flanagan told investors in April 2017 that esure had aggressive growth plans.

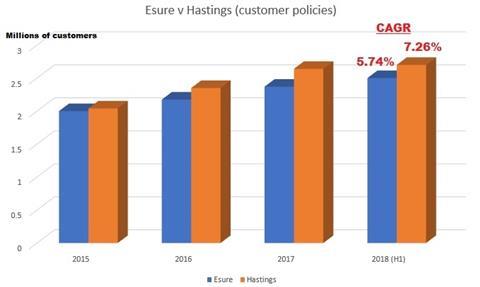

The Peter Wood-founded insurer aimed to clock up three million customers by 2020, with 8% compound annual growth every year.

Esure, Flanagan predicted, was ’running the risk of the perennial boom & bust which so characterises UK motor insurance’.

Flanagan and other analysts, such as Berenberg who warned of the risks, will surely now feel vindicated following esure’s solvency issues.

Esure told the market this month it was working to restore solvency coverage after its level dropped from 155% in 2017 to 110% in 2018.

It is estimated to have rapidly gone through £120m in capital.

Esure cited ’higher than expected claims costs, against a backdrop of lower premiums across the market’ for the solvency issues.

The episode has left rival insurers and market participants asking a range of questions: did Bain know about the issues before buying esure in August last year? What exactly caused the issue? Could something like this happen to us?

Solvency issues uncovered

Competitors have quickly formed their own view of what happened.

One source working at a rival insurer told Insurance Times: ”There was an insurer disrupting pricing in the second half of last year and nobody could identify it. We thought at the time it could have been Esure.

”They’ve piled significant additional volume in the second half of last year, as they have gone into the transaction.

”When you add to the policy count, there are more units and generated capital required.

”And this was done at time when there were indications of under-reserving anyway. It will probably be taken down the Hastings, Admiral route.”

Another source, who has been tracking esure closely for an number of years, believes the red flags were there for all to see for a while.

“It had an aggressive growth target and it was operating outside its core footprint. It wasn’t the real racy stuff such as young drivers and convicted drivers, but it was on the upward part of the risk curve. Esure had typically operated on a more benign customer risk.

Esure, founded by Peter Woods, was bought for £1.2bn by Bain in August last year

”Then on reinsurance they didn’t fully place the coverage,” he said.

However, supporters of esure see it differently.

They dismiss the idea it was pricing too aggressively and suffering a backlash because it took on higher risk customers.

Esure had a gradual ‘test and learn’ approach to its underwriting; there was no cause for worry in the difference between the core footprint and the areas of expansion.

On the pricing, esure last year actually put the brakes on last year, while some competitors took advantage of the government’s claims reforms and expected benefits of the Ogden discount rate reversal.

Although Bain did careful due diligence, it emerged post-deal by natural development that some prior years needed extra provisioning to cope with a handful of claims.

Meanwhile, the 2018 year itself had been a particularly tough one considering the market’s downward pricing combined with higher claims inflation following the bad weather, and continuing higher costs of repair on car and home.

With these claims coming at a time when the esure customer base has grown, decisions are being taken to strengthen the solvency.

Reinsurance was also a factor, as other players have all-encompassing quota share arrangements and more reinsurance cover once individual claims start going into the millions.

A different reinsurance structure for the Bain-owned esure is now being carefully considered, Insurance Times understands.

The possibility of Bain and esure continuing to develop a digitally-advanced and highly-customer focused insurer, away from the continual short-term pressures of the stock market, means the investment remains attractive.

Market pressures on other players

The big question now being asked is whether the issue was specific to esure or will be felt by the wider market.

The 2018 bad weather and soft market could see other players report issues

Berenberg analyst Iain Pearce said in a motor update briefing: ”We view this very much as a company-specific issue.

”As we discussed in multiple notes, we believed esure’s growth and footprint expansion was fraught with risk, especially given its minimal reserving buffers. We do not believe that any of the companies in our coverage have acted in such an ill-disciplined manner.”

However, Pearce believes that those insurers, such as Hastings, that have reined in their pricing last year can potentially reap the benefits as opposed to other players who were more aggressive.

Barclays broadly agreed, saying in an esure note: ”In our view, while at first sight the statement provides negative read-through for the UK motor market, confirming the margin deterioration from declining pricing (confused.com index shed a 6.4% decline YoY in 4Q18) and still high claims inflation at 5-6%, the market should be well aware of that from comments by other listed players.

”At the same time having one of the more aggressive competitors in the market that still grew policies by 13%YoY in 1H18, and earned premiums by 25% to likely retrench to protect balance sheet may allow its listed peers to be more active in passing through claims inflation.”

However, one source, told Insurance Times: ”There will be others who have issues. This isn’t something unique to esure.

“We have already seen some signs of it, but there will be more.”

It may only be February, but once again it appears UK private motor is shaping up for another interesting year ahead.

No comments yet