Funding for insurtechs has historically been a struggle, but industry commentators believe investment opportunities are on the up thanks to the technology focus brought about by the Covid-19 pandemic

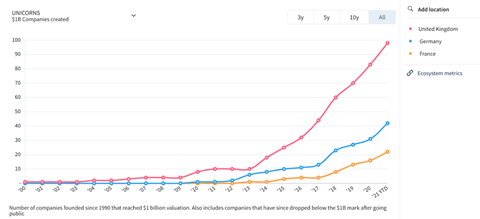

With three unicorns and counting in 2021 so far, the insurtech sector is at the top of its game - June saw the UK become the first country in Europe to hit a 100 unicorn milestone this year, following the valuation of artificial intelligence (AI) company Tractable.

A unicorn is a private technology startup valued at $1bn (£716,425,000) or more.

Although investment reaching hundreds of millions of pounds within one funding round was practically unheard of in the insurtech sector pre-pandemic, GlobalData’s insurance analyst Jazmin Chong told Insurance Times: “There are several factors that flag that insurtech investment is expected to continue growing over the next couple of years.

“More and more tech-centric players in the insurance space are now being able to raise enough funding and reach multibillion dollar evolutions.

“The pandemic has accelerated the demand for digital and personal insurance services - increasing consumer demand for digital services shows no sign of abating.

“The success of insurtechs’ recent funding rounds proves that such startups have been able to insert themselves successfully into the insurance value chain.”

However, GlobalData’s Smart Money analytics tool found that global investment in the insurance industry overall dropped by 17.3% in 2020 compared to the previous year, reaching a total value of $3.5bn (approximately £2.5bn).

Maturing ecosystems

Yoram Wijngaarde, founder and chief executive of startup data provider Dealroom, said: “The raw unicorn figures can be a sign of a maturing ecosystem, but there is also no let up in pace.”

He tipped Europe to be “an entrepreneurial hotbed attracting international investor attention”. In June 2021, the UK had more tech unicorns than Germany (42), France (22) and the Netherlands (18) combined.

Chong added: “When looking at the development of ecosystems, such as the Internet of Things (IoT), insurtechs are betting on [these] in order to go from claims handling, to prevention, to prediction.”

GlobalData found that industrial IoT revenues reached $247bn in 2020, up from $231bn in 2019. GlobalData forecasts these revenues will hit $555bn by 2024, growing at a compound annual growth rate (CAGR) of 19.1% between 2019 and 2024.

“The market consists of various applications, such as advanced automation, asset tracking, conditional monitoring, environmental monitoring, healthtech, people and animal tracking and telematics. All of which will feed into insurtech growth and therefore investment,” Chong said.

Catering to a niche

Speaking about the UK’s three latest insurtech unicorns - Bought By Many, Zego and Tractable - Paul De’ath, head of market intelligence at Oxbow Partners, said: “Each of those businesses is well placed on the back of the pandemic.”

He explained that due to the increase in pet ownership during the Covid-19 pandemic, Bought By Many has prospered with its pet insurance offering. Equally, mobility insurance provider Zego has benefited from the growth in online deliveries and the demand for gig economy workers during lockdown.

Chong pointed out that “certain themes are proving to be more essential since the Covid-19 outbreak”, such as AI. Firms using this technology saw a 6.1% increase in investment in 2020, she added.

De’ath continued: “Companies that can work on the back of being tech-enabled and remote are probably going to do better [moving forward]. Within that are those that are playing to a niche [too].”

However, whether this success continues depends on what happens post-pandemic. “If the backers make lots of money, the next insurtech that comes along might find it easier to get funding,” he added.

Chong agreed, noting that funding is currently more evident for younger insurtechs.

She said: “GlobalData finds that 45.4% of global insurance venture capital (VC) investment has gone to companies in a seed round and series A [funding round] between 2014 and 2020, with insurance companies in series C and D [rounds] attracting only 4.4% and 1.8% of insurance VC investment funding [respectively] over the same corresponding period.

“This flags that the insurtech companies that have captured VC’s attention are only beginning to mature, with an expectation that these newly funded companies will demand further funding as they begin to grow in the coming years. Similar to Zego, which was founded in 2016.”

Space in the market

Despite the undeniable interest in insurtech, Matt Connolly, chief executive of Sønr, noted that ”there are a lot of insurtechs with very similar businesses - there isn’t enough space in the market for all of those to succeed”.

In his opinion, the insurance market is ”going to find the collapse of some, consolidation of others and a lot of acquisition going on”.

”From an acquisition perspective, it’s only going to become a growing trend as companies buy their way towards the future,” he added.

Regardless of potential M&A, De’ath stressed that “there is no going back” to the way things were pre-pandemic within the insurtech sector, thanks to the acceleration of technology innovation and adoption over the last 16 months.

Insurance Times’s timeline of UK insurtech unicorns in 2021 so far

- Zego

Sten Saar, Zego’s chief executive and co-founder, said: “This latest round of funding is a huge milestone for Zego. It is a testament to our relentlessly hard working team and a clear validation of the need for Zego’s products in the market.”

Founded in 2016, Zego specialises in commercial motor insurance. Its insurance offering covers self-employed drivers, courier riders for firms like Deliveroo and fleets. It has also been involved in insuring e-scooters for the UK government’s trials.

- Bought By Many

Its most recent funding round was secured through its holding company, Many Group, and the investment was led by European-based investment firm EQT Growth.

Founded in 2011, the insurtech entered the market in Sweden in 2019 and began a US roll out in March 2021, where it operates under the name ManyPets, offering a subscription-based model for pet health insurance and wellness packages.

Steven Mendel, Many Group’s chief executive, said: “Our mission is to make the world a better place for pet parents.”

- Tractable

June 2021 also saw Tractable gain unicorn status following a series D fundraise of $60m, led by venture capital firm Insight Partners and fintech company Georgian, making the artificial intelligence (AI) specialist the third unicorn this year in the insurtech sector.

This funding round doubles the total raised so far by Tractable from $55m to $115m and values the company at $1bn.

Alex Dalyac, Tractable’s co-founder and chief executive, said: “We’re proud to be the UK’s latest unicorn and the world’s first computer vision unicorn for financial services.”

Tractable was founded in 2014 and uses AI software to view and assess images of vehicle damage for faster claims processing.

No comments yet