Saga underwriter Acromas cuts its combined operating ratio to 36%, while AA scores biggest improvement in loss ratio and Acasta returns to a stable solvency position after reporting a sub-100% solvency coverage ratio

More than half of the 23 Gibraltar-based insurers that were analysed in this report reported an underwriting profit in their most recent Solvency and Financial Condition Report (SFCR).

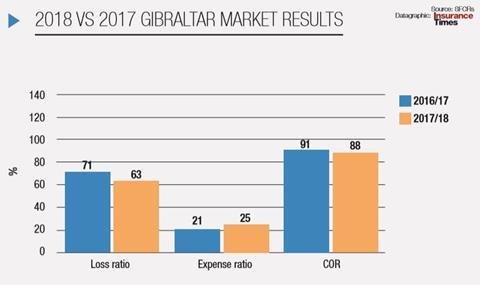

An Insurance Times analysis of the SFCRs for the Gibraltarian general insurance market revealed that 14 insurers reported a sub-100% combined operating ratio (COR), resulting in an aggregate COR for the market of 88%.

This is an improvement of three percentage points compared with the previous year, when the aggregate position was 91%, largely driven by an eightpercentage-point loss ratio improvement.

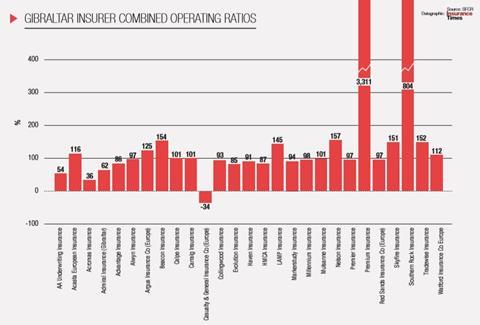

Saga underwriter Acromas Insurance was again the top-performing Gibraltarian insurer with a COR of 36%, down 10 percentage points from 46% last year.

More than 99.9% of Acromas’s premiums came from the UK, the rest from Ireland, but the decision to stop writing business there on 30 June 2017 means that the insurer will be solely focused on the UK.

Most of this business comes from the motor insurance market, with 75% of all risks ceded to reinsurers through a threeyear quota share reinsurance treaty signed in early 2016.

The highest COR in this report comes from Premium Insurance, with a reported COR of 3,311%, although this is largely due to the low premium base from which the insurer is operating.

The insurer only started writing business in December 2016, focusing on Slovakian industrial and commercial property and commercial liability business. In 2017, the insurer achieved net earned premiums of just £28,000, having been “unable to offer terms to brokers in time to write January business, which is a major renewal season in Slovakia”.

This resulted in “significantly less premium being written in 2017 compared to the original plan”, according to its SFCR. Managing director Andy Baker told Insurance Times that the insurer had a three-year plan that would lead it into profit after continued premium growth.

“We are still in an early phase of our start-up, and our three-year plan includes strong top-line growth, higher risk retention, stable expenses and a tipping point in 15 months’ time,” he says. “It will be great to record a profit and it will be, more or less, in line with the original forecasts.”

Risk mitigation

Of the established insurers, Southern Rock had the highest COR, with a loss-making 804% on a net earned premium base of £7m.

Head of finance Mathew Ruiz told Insurance Times this figure was not representative of the insurer’s true performance given the nature of its reinsurance arrangements.

“Southern Rock’s risk mitigation strategy has continued its use of reinsurance cover and loss portfolio transfer (LPT) arrangements, all with A-rated or higher reinsurance partners,” he says.

“The use of reinsurance and LPT means the company has effectively reduced its exposure to claims to just 3% of written premium each underwriting year since 2014.

“On a statutory accounting basis, Southern Rock reported a profit on its technical account of £2.6m for 2017. The overall loss for the year after tax was £4.3m.

“On an underwriting basis, however, ie after removing the impact of accounting deferrals, such as deferred acquisition costs and statutory reporting requirements for LPT arrangements, Southern Rock’s underlying business remains profitable: the underwriting profit for the year before tax was £2.3m.”

Ruiz adds: “The ratios are not truly reflective of the performance of Southern Rock, due to the benefit of reinsurance commission income not being included. This income is a fundamental part of the Southern Rock business model.”

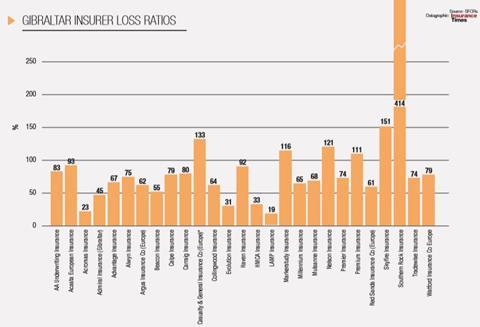

Southern Rock’s loss ratio of 414% was also the highest in this report, while Skyfire Insurance reported the second highest. Skyfire delivered a loss ratio of 151% on net earned premiums of £28.5m, but a Skyfire spokesperson said the result was skewed by the impact of reinsurance arrangements.

“All of Skyfire Insurance Company’s excess of loss outward reinsurance premiums are booked to the technical account in its financial statements, whereas the proportionate commission from Skyfire’s Quota Share partners to offset this premium is reflected as a contribution to operating expenses. This has the effect of overstating the calculated COR – the actual underlying net claims ratio is 81.2%.”

In its SFCR, the insurer said the bulk of its profit was “derived primarily from its share of the group’s non-technical income”.

Overall, only nine insurers managed to reduce their loss ratio over the last 12 months, but the best in this analysis was achieved by Lamp Insurance, which writes a variety of niche products across the globe, including legal expenses, medical expenses, miscellaneous financial loss and fire and other damage to property.

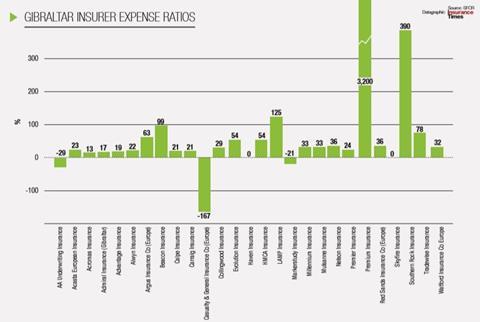

The insurer reported a loss ratio of 19%, although high expenses resulted in an expense ratio of 125%, pushing the insurer into loss-making territory for the year with a COR of 145%.

AA Insurance was the most-improved insurer when it comes to loss ratios, largely benefiting from an increased premium base in its second year of writing business.

The insurer wrote net earned premiums of £9.3m for the year ending 31 January 2018, compared with £1.6m for the previous year. This helped the insurer reduce its loss ratio by 58 percentage points to 83%, down from 141% in 2017.

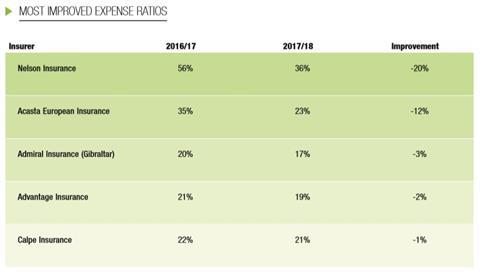

Only five insurers managed to improve their expense ratio, with Nelson Insurance reporting the most improved, knocking 20 percentage points off its expenses to achieve a ratio of 36% for 2017/18, down from 56% the previous year.

This improvement comes after Nelson slimmed its expenses by one-third to £4.1m, while at the same time growing net earned premiums by more than 5%.

Solvency II capital issues

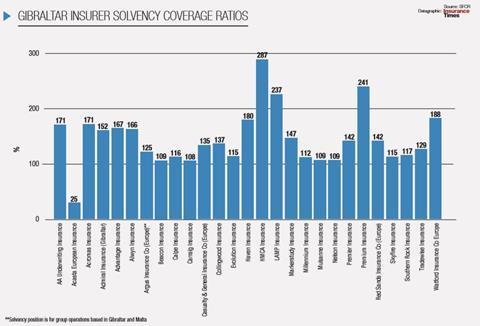

With Solvency II transition periods coming to an end, all but one insurer managed to report a solvency coverage ratio (SCR) above the 100% threshold for 2017/18, compared to four in 2016/17.

Furthermore, last year’s inaugural Gibraltar Insurers report concluded that a further eight insurers were found to have an SCR only just above the 100% cut-off (less than 105%), whereas this year all insurers reporting a compliant solvency position achieved an SCR above this 105% barrier.

Acasta Insurance was the only insurer to fail to meet the 100% barrier laid down by Solvency II, reporting an SCR of just 25%, even failing to meet its minimum capital requirements, reporting a minimum coverage ratio (MCR) of 57%.

In its SFCR, Acasta said: “A small number of books of business deteriorated during the year and corrective action was taken. This, together with a requirement to strengthen reserves, resulted in a significant stress on solvency arising at the end of the year.

“During 2017 the relationship with the outsourced insurance manager deteriorated. A replacement manager was appointed at the end of the year.

“The Board took action to review controls in place and instigated an overhaul of how our financial information is produced, with the aid of its new insurance manager from December 2017. The integrity of financial and solvency reporting has improved and the Board has regained confidence that the management information produced is an accurate reflection of the company’s position.”

Acasta operations director Andy Shaw told Insurance Times that a remediation plan put in place by the insurer has already seen improved solvency that has taken the insurer’s funds back above the 100% threshold under Solvency II.

“The remediation plan consists of a whole book quota share from 1 January 2017 to 31 December 2018, 100% quota share of all years of the French construction book, withdrawal from the French construction and rental guarantee markets and £5m of capital injected by the shareholders,” he says. “The effects of these actions were that the company reported a SCR solvency ratio of 117% and an MCR ratio of 468%, at 30 September 2018.”

Overall, however, the solvency position in Gibraltar has improved considerably over the last 12 months.

Protecting customers

Gibraltar Financial Services Commission (GFSC) chief executive Samantha Barrass says it is the ongoing protection of customers that drives its approach to regulation.

“The GFSC’s regulatory and supervisory approach is driven by our statutory objectives to protect consumers and the reputation of Gibraltar,” she says. “That is our priority. As with the UK and other regulators, the GFSC does not operate a zero-failure regime, which is one of the main characteristics of a free market. What is important is how we deal with failure, ensuring that we do what is necessary to protect consumers and the market as a whole.

“While financial strength ratings can be a useful barometer of the financial health of a firm, this does not in and of itself prevent rated companies from failing. This can still happen to both rated and unrated insurers.”

The regulator continues to put procedures in place to better prepare should a collapse happen, such as the failure of Horizon Insurance when it entered administration in December 2018 after three years of being in run-off, and has even launched a thematic review.

“Studies of collapses or near-collapses during the financial crisis identified poor governance and lack of experience or staff knowledge as two main reasons for corporate failures,” Barrass says.

“Our approach centres on ensuring that firms have both appropriate financial and non-financial resources. Given the importance of governance we have launched a Corporate Governance Principles Thematic review.

“We also require firms to hold a suitable buffer over the Solvency Capital Requirement mandated by Solvency II.”

Barrass says the GFSC has also introduced further measures to better protect customers.

“In 2017, although not required by EU regulation as of yet, we implemented a requirement for firms to consider recovery plans (similar to those required by banks) as part of the forward-looking solvency assessment,” she says. “Firms need to consider the stresses they could experience and how they would recover from any such stresses, the ease of, and barriers to, implementing any solutions, and the availability of additional capital if needed.

“Firms also need to consider early warning indicators of potential problems. By carrying out this exercise on an annual basis, and documenting this in the firms’ own risk and solvency assessments, firms should be well prepared to deal with unexpected issues and the types of market stresses which can occur.”

No comments yet