Howden has become a huge player in the UK commercial market with its Aston Lark deal, but there are risks

By Content Director Saxon East

Step aside Gallagher, there is a new giant on the block.

Howden’s purchase of Aston Lark is a watershed moment for UK retail broking M&A.

Trade sales of UK commercial brokers have been dominated by the mega-brokers of America - Marsh, Aon, Willis and Gallagher.

Ardonagh has made some big individual purchases, but nothing on this scale in the UK’s SME broking heartland.

Howden has now stepped in as a major player with its acquisition of Aston Lark.

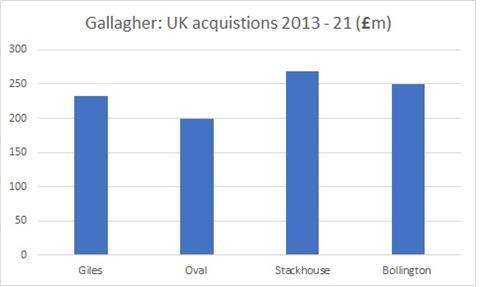

It paid £1.1bn for Aston Lark, a figure which is more than all of Gallagher’s major purchases in the UK since 2013 (see below).

This comes a year after paying more than £600m for A-Plan.

Yet these acquisitions are not without risk.

Howden risks

The deal for Aston Lark was on a 17-18 reported earnings multiple.

It is important to remember that there is an ‘ebitda bridge’ - so the multiple will have future earnings of Aston Lark’s recently acquired businesses baked into it.

Furthermore, there can be cost savings once the Aston Lark business is integrated.

This means the actual multiple will be lower than what has widely been reported.

Nonetheless, the figure looks high in comparison to other deals.

Is David Howden making aggressive purchases right at the top of the market? Or will these turn out to be wise purchases?

Howden has a £2.4bn debt, meaning its debt to ebitda ratio is between seven and eight, according to bond credit rating business Moody’s.

It recently gave Howden a B2 rating on its loans. This refers to speculative grade debt that is ”subject to high credit risk”.

Looking at the bigger picture, rises in interest rates and a choking up of credit markets could leave the business in a difficult position.

There is also execution risk in all these acquisitions.

Howden has to integrate its major purchases, such as A-Plan and Aston Lark, which themselves have made multiple acquisitions.

On the plus side, Howden has a track record of making acquisitions and continuing to be a highly cash generative business.

The broking group produces healthy, positive free cashflow.

A high proportion of the equity is still owned by staff, boosting workforce morale.

In summary, Howden looks strong right now, but these highly-leveraged acquirers have their risks and can find themselves at the mercy of the wider market.

No comments yet