Insurers will be challenged with how they respond to the polarising impact of the coronavirus pandemic, and they must not fall into the trap of excluding a large swathe of vulnerable customers from their books of business

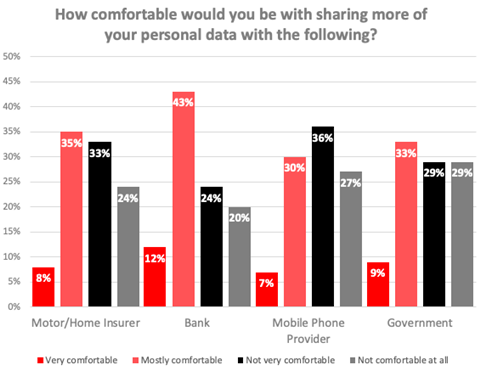

More than half of motor and home insurance customers are not comfortable sharing data with their insurer, according to new research from Consumer Intelligence.

The research found that only 43% of those surveyed were comfortable with sharing data with their insurer, and consumer intelligence chief executive Ian Hughes says it is clear that the Covid-19 pandemic has had a polarising effect on consumers.

“People are using data services more than ever, but the world is becoming increasingly polarised on this issue,” he says. “You have about a third of people who are data savvy and understand that their data is valuable and are protective of that, and then you have quite a few people who are saying they don’t care as long as there is something in it for them.

“This polarisation means that insurers really have to think things through.”

And when it comes to what consumers want in return for their data, the answers are clear.

The Consumer Intelligence survey found that more than two-fifths (42%) of respondents said that they would be more willing to share data if they had more personalised pricing in return, with 30% wanting greater protection in case of accidents or emergencies.

Other popular initiatives that consumers said would make them more willing to share data include personalised offers or incentives from other providers (22%) and a more personalised service from their insurer (21%).

Despite this, more than a third of consumers (34%) said there was nothing that insurers could offer that would make them more willing to share their data.

More needs to be done

And Hughes says that this polarisation effect also creates an ethical dilemma for insurers to grapple with.

“If those people who don’t want to share their data are vulnerable customers, then insurers are effectively doing something that is adversely affecting vulnerable people [by using this data to tailor pricing],” he says. “So more needs to be done to understand those dataphobes and why they don’t want to share their data.

“Is it because they are vulnerable and don’t understand the process, and therefore could see themselves excluded from credit or insurance, so that only those who are data agnostic and don’t mind sharing their data have access to better prices and better products.”

All of this means insurers need to be very careful with the approach they take to using data to price risks, particularly in the post-coronavirus world where consumers may be more confined to two opposing camps with regards to data sharing.

“There is a real need for insurers to look at risks and see if there is a relationship between people willing to share data and claims,” Hughes says. “Otherwise we may end up isolating or excluding a load of people from cover, not because they are a bad risk, but just because they don’t want to give up their data.”

Flexibility

To combat this, Merlie Calvert, founder of legal services firm Farillio, says insurers need to adopt a more flexible approach when designing their policies.

“Insurers should be looking to have more of a graduated relationship with consumers, rather than the on-off relationship you see at the moment,” she says. “If you look at what a customer needs right now, it is the ability to have much more flexible insurance. So on the days when a customer is not working, or like now with many businesses still not operating because of the lockdown restrictions, insurers can give them the option to turn down the level of cover they have.

“Inevitably, insurance has to get more instantaneous instead of being renewed once a year at renewal.”

Hughes says that trust could be an issue for insurers looking to have this more in-depth and data-led relationship with their customers, but that there are emerging options out there for insurers to combat the reputational problem insurers have.

“The reason why people won’t share data is because they dont trust insurers,” he says. “But there are models coming out of the US and other areas where there is a trusted third party who consumers share their data with and the insurer is then given enough access to that data to get what the consumer needs, but not too much that they feel it can be used against them.

“Insurers need to look to work with trusted partners so they can get access to the data to determine if someone is a good risk or not.”

And Merlie says that by getting this right, insurers will have happier and more loyal customers.

“If you look at the best corporates and the best businesses, they have regular interactions with their customers,” she says. “So they know what is keeping them happy and what they are not happy with.”

Read more…Supporting vulnerable customers- a great opportunity for insurers to rebuild reputation amid Covid-19 crisis

Not subscribed? Become a subscriber and access our premium content

No comments yet