Digital transformation within claims departments is accelerating – and insurers are employing different approaches to tap into the relevant tech expertise to improve customer and cost outcomes

Making a general insurance claim in the modern era of artificial intelligence (AI) and machine learning means it can be a very different experience today compared to just a few years ago.

Ian McKenna, founder of the Financial Technology Research Centre (FTRC), said: “Technology is having a huge impact on claims being paid more quickly and identifying those that need further investigation.

“The call centre you’re talking to is often using biometric technology to measure the stress in your voice, to identify whether you’re telling the truth or not.”

The claims sector has been playing catch up when it comes to digital transformation, with virtually every aspect of it now undergoing a high-tech journey – featuring everything from self-service apps to drones.

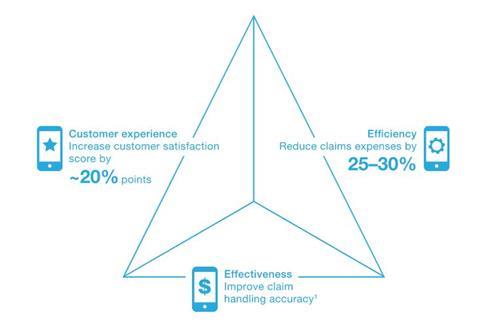

A McKinsey and Company article published in April 2018 – entitled Claims in the digital age: How insurers can get started – noted that “for the property and casualty industry, digitising the claims function holds tremendous potential”.

It continued: “At the core of the claim function’s digital transformation is a redesign of the claims customer journey.

“There is no silver bullet interaction that ensures customer satisfaction, but a successful redesign typically involves considering processes from the customer perspective and optimising back office processes accordingly to provide simple and fast claims services.”

Ben Goldring, head of financial services at FinnCap Cavendish, agreed with this sentiment.

He explained: “Claims are not the dirty back end of the insurance process, but the point at which you actually deliver to your customers.

“During [the Covid-19 pandemic], there was a real turning point as people were finding [submitting] claims [to be] a very tricky process.

“AI and automation tend to work well with high volume, low value claims where the efficiency gains from automation outweigh any drawbacks from not having more human interaction.”

In addition, there is increasing industry focus on using technology – like the Internet of Things (IoT) – to prevent future claims from occurring, as well as a growing realisation that the claims journey does not simply stop at the resolution stage.

Lisa Bartlett, president for UK and Ireland at Crawford and Company, said: “A lot of valuable data collected on [the claims] journey can be combined to better understand critical loss trends that can better inform the client.

“These data insights must be captured and fed back to ensure that [firms are] continually able to explore ways to further optimise the claims experience.”

Cost impact

However, technology isn’t just about pure innovation. Some tech is helping to gradually evolve processes like cost reduction.

A Deloitte Insights article, published in October 2021, noted that “the pressure is always on to augment claims processing with new technologies and data sources that can increase efficiency, productivity and accuracy, since every dollar saved goes straight to the bottom line”.

“Claims is by far a property and casualty insurer’s biggest cost component,” it added.

Similarly, a March 2017 report from McKinsey and Company – entitled Digital disruption in insurance: Cutting through the noise – found that although “insurance has been relatively slow to feel the digital effect, owing to regulation, large in-force books and the fact that newcomers seldom have the capital needed to take insurance risk on to their balance sheets”, the sector “is not impregnable” to technology transformation.

Read: In Focus - Digital transformation in the claims arena is no ‘panacea’

Explore more insight articles here.

The report cited that “automation can reduce the cost of a claims journey by as much as 30%”.

Olly Laughton-Scott, managing partner at Imas Corporate Finance, noted: “Claims businesses have been taking out costs from the claims process for many years and automation has always played an important part in this.

“Arguably, smaller, specialist businesses can do a better job in this respect as insurers find it harder to innovate.”

Insurer activity

To better reap these benefits of technology within claims departments, some incumbent insurers have focused on developing in-house technological capabilities.

Gerry Glombicki, senior director at Fitch Ratings, said: “In-house is obviously the cheapest way to go, but also the most difficult as companies may not have the expertise to actually solve the problems.

“Recruiting this [expertise] can be costly and there are no guarantees it will work.”

Other insurers have been partnering with insurtechs or other technology suppliers.

For example, Sprout.ai has been working with several general insurers on claims automation, such as Zurich Insurance UK. Using advanced AI, the insurtech can help reduce the time taken to process a claim from an average of 30 days to near real-time.

Investing in external parties has also provided some insurers with a way of strengthening insurtech relationships.

For example, in May 2022, Intact Ventures – the venture capital arm of RSA’s parent company – led a £16.5m funding round in Urban Jungle, which uses fraud modelling within its claims function.

Insurers that invest in startups or later stage digital growth companies have become quite extensive.

For example, Allianz X – which invests in digital front runners in ecosystems relevant to insurance and asset management – already has 25 scaleups in its portfolio and boasts assets under management of over €2bn (£1.7bn).

Other players have been importing technology expertise by going the whole hog and making acquisitions, although – as with investing opportunities – claims-centric firms are not featuring any more prominently in M&A pipelines than other parts of the value chain.

Only two out of the eight acquisitions made by Davies Group during the last year were of claims solutions companies, for example – ProAdjust in June 2022 and Building Validation Solutions (BVS) in December 2021.

Read: Briefing - Commercial lines digitalisation now ‘accelerating’ after slow start

Read: Technology implementation is ‘do or die’ for insurance sector

Explore more insight articles here.

But, with insurtechs in particular, the impending economic downturn may see M&A increase in significance as a way of securing external expertise.

Matt Connolly, chief executive of Sønr, explained: “We are coming into an interesting period as insurtechs will not necessarily get the venture capital they need to fund their business models, so they may become available for sale very cheaply.

“During the next 12 months, incumbent insurers may, therefore, be buying insurtechs across the board, including those involved with claims.”

Many roads to end goal

No single approach to acquiring claims technology is currently holding sway over other methods and, in practice, insurers tend to combine different strategies.

Technological progress in the claims area alone has also not gained insurers massive overall competitive advantages so far – but this could change.

Volker Kudszus, sector lead of insurance ratings at S&P Global Ratings, said: “It’s not important to us whether high tech claims capabilities are being developed internally or coming from external partnerships or via acquisitions. It’s the result that matters and ineffective claims processes result in an extra cost which could eventually affect a company’s margins.

“In a few years’ time, those insurers not up to speed with digitalisation could lose market share. But no insurers are denying this is a mega trend, so if any fall behind, it won’t be through ignorance.”

No comments yet