Acquisitional growth has forever changed UKGI’s broking landscape, however market feedback indicates that there is a fine line between consolidation creating both customer and colleague benefits, or actually working against the industry’s best interests

When in conversation with this month’s (April 2026) cover star, Daniel Lloyd-John – chief executive at Manchester broker Broadway Insurance Partners – we mulled over the entrenched trend in UK general insurance (UKGI) around insatiable broker consolidation.

This activity has had a marked impact on UKGI’s broker landscape, with consultancy MarshBerry confirming last December that “the value of sector deal activity in 2025 is likely to be the lowest since at least 2019” because “years of consolidation have hollowed out the number of privately-owned mid-sized brokers available to acquirers”.

MarshBerry UK managing director John Nisbet predicted that the number of fully authorised broking groups in the UK currently stands at around the 2,000 mark – or nearer 3,700 if including appointed representative (AR) firms – with the next “plentiful, albeit gradually diminishing” pot of M&A targets being brokers with 10 staff or less.

While acknowledging that intermediary M&A is “part of the circle of life”, Lloyd-John is also adamant that “consolidation is not good for customers 99% of the time”.

In his view, this is because “there becomes a point when the world’s largest broking propositions fail to resonate effectively with an audience”.

He told me: “[This] is simply because that organisation has got too large [so] that it has forgotten how to interact quickly and effectively between itself. [Therefore,] two things creep in – inconsistency and complacency.

“My fear for consolidation is that it might affect the reliability, complacency and consistency of what [the] regional broker dynamic really thrives on, which is closeness and relationship driven retention.”

Lloyd-John, therefore, is “obsessed” with calculating what the optimal size of a retail broker is – before scale driven inconsistency and complacency “creep in”.

Clout, consistency and client care

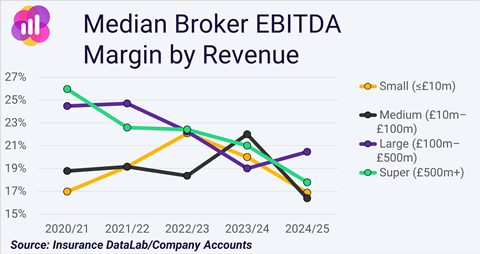

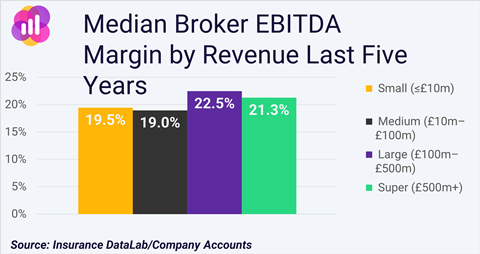

Insurance DataLab co-founder Matt Scott has a good idea of how he would define this “sweet spot”, however, identifying a broker band that does align with Lloyd-John’s thought process.

Scott ringfenced the “upper mid-market” – brokers with between £100m and £500m in revenue – as the cohort “where profitability, consistency and productivity all come together”.

He explained: “The data does not show that bigger automatically means better. When you look across five years of financial results, margins don’t just keep climbing as firms get larger.

“In fact, the £100m to £500m brokers have delivered the strongest median profitability over [this reporting] period – slightly ahead of the very biggest groups.

“What’s also interesting is productivity. Revenue per employee peaks in that £100m to £500m band, not at the very top. That suggests there may be a point where [firms have] captured the benefits of scale – systems, insurer leverage, specialisation – before organisational complexity starts to weigh on efficiency.”

Scott does not think that a single, perfect size of broker exists – but he contrasts Lloyd-John by flagging that scale does provide consistency, with the largest firms not really reaping losses and performance generally meeting expectations. “Scale seems to smooth things out,” he added.

Read: Chief executive remains ‘sceptical’ over insurers’ ability to integrate startup acquisitions

Read: ‘Centre of gravity’ of European M&A market shifting out of UK – FTI Consulting

Explore more M&A related content here, or discover more news here

Linking the question of optimal broker size back to M&A, Jeremy Riley – senior advisor of the UK insurance practice at FTI Consulting – noted that “in the current M&A market, problems tend to arise when a business grows faster than its ability to integrate its acquisitions”.

He continued: “When this happens, operating costs rise, synergies fall short and customer experience deteriorates.” This reflects the size linked line in the sand that Lloyd-John mentioned.

For Riley, the post-acquisition integration process is vital in protecting against the inconsistency and complacency Lloyd-John noted. He explained that scale advantages such as “broader market access, greater negotiating power and deeper specialist expertise only materialise when there is a clear, coherent, disciplined operating model”.

He added: “When local entrepreneurial businesses are flattened into a single, generic structure it can add bureaucracy, slow decision-making and damage client service. Successful consolidators recognise this and invest heavily in integration, while preserving the core strengths of the business they originally acquired. They build in-house specialty divisions and regional hubs that retain their sector or geographic focus, have strong local leadership and tailored service models.

“Ultimately, the ‘right’ size [of a broker] is large enough to invest and small enough to stay close to clients – operating across specialties and borders, but structured around client focused teams with a real commitment to delivering to the best outcomes.”

Broker M&A in recent years has fundamentally shifted the shape of the UK’s intermediary marketplace. The large are getting larger, startups are springing up and what is left of the mid-market is teetering on the cusp of consolidation – whether in the UK or further afield.

Lloyd-John has issued a market-wide warning that large scale consolidation can be detrimental to customer care – but how closely is this monitored by buyers when acquisitional growth can be an attractive bottom line addition?

Size seemingly does matter – but the see-saw of scale benefits and efficiencies versus potential inconsistency and complacency have yet to successfully balance out to the market’s satisfaction.

Since joining Insurance Times, Katie has successfully obtained a number of industry accolades. At trade body Biba's 2025 Journalist and Media Awards, for example, Katie was named the overall winner and received the Journalist of the Year trophy, alongside the Best Thought Leadership Award for her briefing article on reproductive health MGA Juniper and how insurance can be used to positively impact taboo subjects.View full Profile

No comments yet