Following the news that unrated Danish insurer Gefion has gone into liquidation after its licence was revoked, Insurance Times takes a look at five of the biggest insurance disaster stories of the last 20 years

Gefion has become the latest insurer to enter liquidation after the Danish Financial Services Authority (DFSA) refused to extend the insurer’s recovery period and revoked its insurance licence.

The news followed a period of emphatic growth for the unrated insurer, but also concerns that claims would follow close behind and that Gefion was over-stretching its capital position.

The DFSA was also concerned, ordering Gefion to stop writing new business from March 2020, and ultimately shutting down the business just three months later.

But Gefion is by no means the only insurer to fail over the course of the last two decades, so here is Insurance Times’ round-up of the five biggest insurer collapses.

5. LAMP

In 2019 LAMP became the latest Gibraltarian insurer to file for liquidation after it failed to secure additional funding to restore its solvency position.

One of the biggest problems for LAMP was its inability to control costs, with the Insurance Times Gibraltar Report 2019 revealing that the insurer reported the third highest expense ratio of the Gibraltarian insurers analysed at 125%, pushing it into loss-making territory for 2018, with a combined operating ratio of 145%.

Despite this, the insurer’s solvency position appeared healthy, coming in with a solvency coverage ratio of 237%.

Operating within a niche business model can, however, create cash-flow issues.

The insurer’s Solvency and Financial Condition Report (SFCR) showed that LAMP did put measures in place to manage its liquidity risk, but these proved inadequate.

Analysis of LAMP’s SFCR revealed that almost three quarters of the insurer’s value was held in insurance and intermediary receivables that it expected to be paid.

And LAMP’s healthcare business was particularly affected by its liquidity issues.

The Law Gazette reported that the insurer owned a fifth of the after the event (ATE) clinical negligence market, and that it was caught up in a three-year battle with the NHS over the proportion of damages to be recovered from defendant NHS trusts.

A solicitor told the publication that it was the “dogmatic approach” taken by the NHS that had created a funding hole for the likes of LAMP and put pressure on the whole ATE market.

Ultimately these liquidity issues proved fatal, and the insurer collapsed in May 2019.

4. Alpha

Another unrated Danish insurer, Alpha was declared bankrupt in May 2018 after its reinsurance provider, CBL Insurance Limited, ran into solvency issues.

New Zealand High Court documents revealed that CBL Insurance was the quota share reinsurer for Alpha on French construction, but the reinsurer was massively under-reserving for French construction surety.

When the Danish regulator found this out in July 2017, it ordered Alpha to boost reserves and the insurer was ultimately unable to meet its solvency requirements, ceasing to write new business in March 2018 before filing for bankruptcy two months later.

The collapse led to thousands of cabbies being unable to work as they no longer had any cover, and, ironically, it was Gefion that stepped in to be a capacity provider for Cover My Cab after it picked up Alpha’s cancelled policies following the insurer’s collapse.

3. Enterprise

Back in Gibraltar, Enterprise makes it into our top three after it was declared bankrupt in July 2016.

Gibraltar’s Financial Services Commission (FSC) ordered Enterprise to stop writing new insurance contracts immediately after the insurer advised it that it was insolvent and had been unable to secure additional funding.

The insurer had been on the regulator’s radar for some time in the run up to its collapse because of concerns about its financial position. The regulator had also been seeking assurances from the company about its financial position.

FSC chief executive Samantha Barrass said at the time: ”We have been working closely with Enterprise since the beginning of the year.

”We have been working with the company using the new powers available to the Commission under Solvency II to ensure the Commission has the right information to support our supervision.

”The situation demonstrates the importance of receiving independent verifiable information. This has enabled us to act promptly avoiding unnecessary harm to policyholders.”

The regulator’s director of legal, enforcement and policy, Peter Taylor, added: “The Commission initiated action against Enterprise at the beginning of July.

”The company has endeavoured to find a way out of its predicament but has not been able to do so. Once we had seen the outcome of the independent review of Enterprise’s position Enterprise advised the Commission it was insolvent.

“We have moved very quickly to ensure that we take all reasonable steps to safeguard the position of existing policy holders. This is an inevitable but unfortunate outcome for all concerned.”

2. Gable

Unrated Gable’s troubles came to a head in July 2016 after it stopped writing new business amidst ongoing solvency issues for the Liechtenstein-based insurer.

The insurer said it had instructed its brokers to stop writing business with immediate effect in order to plug a £59m Solvency II shortfall.

The insurer also announced plans to transfer all its UK business and the majority of its European business to rated carriers using managing general agents, allowing it to retain enough capital to operate as a significantly smaller, niche business.

This was ultimately unsuccessful, however, and the insurer was put into administration in October 2016 with PwC taking overall control of the company. Just a month later, and Gable was declared to be in default.

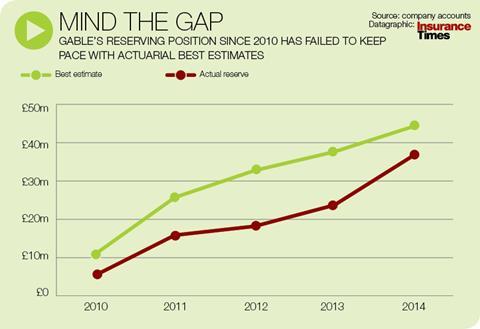

The revelations would not have come as a total shock for the industry, however, as the insurer had been struggling with reserving issues for some time.

Insurance Times analysis of Gable’s financial results revealed that its reserves had consistently been below actuarial best estimates, with the insurer citing niche and diversified business lines as a reason for holding back less than recommended in reserves to pay future claims.

In 2010, Gable’s reserves fell short of actuarial best estimates by 47%, and although this improved over subsequent years, the gap still stood at 17% come 2014, even after Gable pumped £6.3m into prior-year reserves.

1. Independent

The collapse of Independent was the obvious choice to top our list, with the trail-blazing insurer shocking the City and the whole insurance market when it went under in 2001.

Led by the enigmatic Michael ‘Brighty’ Bright, famed for his lavish parties, annual cricket matches and ‘fun, fun, fun’ approach to insurance, the insurer was the new kid on the block that was taking the industry by storm.

In 1993, Independent even became the first general insurer since the end of World War II to float on the stock market, with Bright putting £50,000 of his own money into the business.

Fast forward to the company’s collapse eight years later, and Brighty’s holding was worth £60m.

But shocking as Independent’s demise was at the time, scratching under the surface reveals an all too familiar story.

Over the course of Independent’s last four sets of financial results, the insurer’s gross premiums almost doubled from £438m to £830m, but outstanding claims reserves remained relatively flat, climbing by just 5% from £354m in 1997 to £372m in 2000, meaning that Independent had to turn to expensive reinsurance cover in order to meet its liabilities.

And as well as having a long history of growing successful businesses, Brighty also had a history of over-stretching reserves and pushing through the ‘hard-sell’ with his sales forces, undercutting competitors in order to make the sale and boost profits.

At Orion, the insurer he joined at the tender age of 23, Bright kept climbing the corporate ladder until he was the man responsible for growing the insurer’s national sales force, instilling an aggressive sales policy that would eventually come home to haunt the up-and-coming insurer.

Claims in Bright’s unit began to climb, however, and liabilities became so large that eventually the firm’s auditors advised Orion to close the division to new business, but by that time Brighty had moved on and was already plying his trade at Lombard Elizabethan.

Here too, Bright sought an aggressive sales strategy, encouraging his sales teams to push the hard sell, while simultaneously cutting reserves in order to boost company profits.

This was the same strategy he deployed so successfully in the early years of Independent, but eventually, and unsurprisingly, caught up with him in the end, and led to the ultimate failure of his £1bn business empire.

Read more…Poor data hampering FSCS from tracing customers of collapsed unrated insurers

Not subscribed? Become a subscriber and access our premium content

No comments yet