UK brokers still lagging behind their European counterparts when it comes to profitability

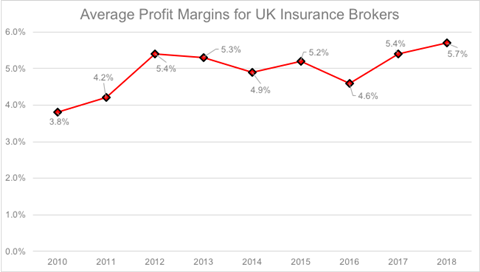

UK insurance brokers have reported an increase in profitability, according to the latest research from Plimsoll Publishing, with profit margins climbing 0.3 percentage points over the last year to 5.7%, representing the second successive year of improved performance.

Speaking to Insurance Times, Plimsoll senior analyst David Pattison said that a lot of this success is the result of ongoing investment in the technology supporting these brokers, and the efficiency savings this can offer.

“There are various drivers behind the changes we are currently witnessing in profit margins, but a key one is that many UK companies have invested heavily in technology in order to drive up productivity,” he said. “This investment in turn is helping to drive growth as brokers improve their market position through efficiencies and look to grow through acquisition.”

Size matters

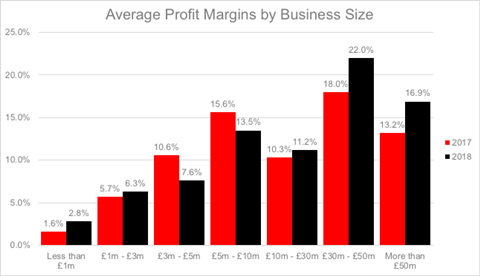

These figures only paint half the picture, however, with the size of the broking firm playing a large part in their profitability.

The research by Plimsoll found that profit margins had increased for the majority of insurance brokers, but that those with sales of between £3m and £10m actually saw a decline in their profitability over the last 12 months.

Pattison said this is largely down to the growth aspirations of these mid-market firms.

“What we typically see is that mid-sized firms are very focused on growth,” he said. “Once companies have become larger, the focus becomes more about maintaining their market position, whereas mid-sized firms are hungry to keep growing.

“Often this means they are spending more on infrastructure, acquisition or recruitment and this reduces profit margins in the short term, albeit hopefully setting them up for success in the medium to long-term.”

Larger brokers, meanwhile, have been looking to reduce costs and prepare themselves for the disruption that could be caused by the UK’s departure from the European Union, currently pencilled in for the end of October.

“We are seeing that many larger companies, particularly those in markets such as insurance or those linked to financial and professional services, are being very prudent due to political uncertainties on the horizon,” Pattison said. “Larger companies are particularly exposed to Brexit, and many are trying to reduce and hold back on costs so as to increase profits and cash reserves.”

Home and motor under pressure

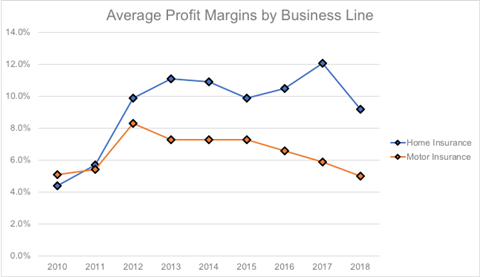

While insurance brokers may have largely been experiencing an uptick in profitability in recent years, the home and motor markets have not been so successful.

The average profit margin for motor brokers has fallen to 5% after peaking at 8.3% in 2012. Brokers operating in home insurance, meanwhile, have seen profit margins fall 2.9 percentage points over the last 12 months, although it still stands at a respectable 9.2%.

Pattison said that the commoditisation of these areas of the market have forced the industry to focus on discounts and price reductions to attract new customers, but at the expense of a weaker bottom line.

“We’re generally seeing companies focus on sales over profit,” he said. “Markets are tightening, especially for consumer products or services with a broad market – of which car and home insurance are good examples.

“Therefore companies have increasingly been using discounts, incentives or price reductions in recent years to retain and attract consumers, which is ultimately having a negative impact on the bottom line.”

UK lags behind European rivals

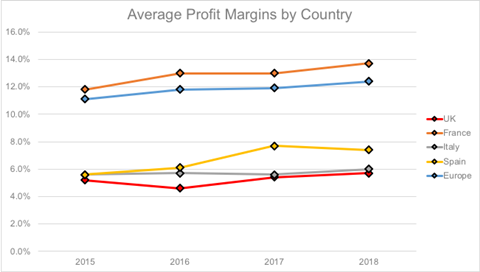

The Plimsoll research also found that UK brokers are lagging behind their European counterparts when it comes to profitability.

UK brokers had the lowest average profit margin of the four countries analysed, with brokers in France reporting profit margins of more than double the UK average. Europe as a whole was also well ahead of the UK, with an average profit margin of 12.4% (UK: 5.7%).

Biba head of compliance and training David Sparkes said that UK brokers have always been at a disadvantage to their European neighbours as a result of the increased costs of compliance in the UK.

“Biba’s commissioned research on the cost of regulation (due to be re-run later this year) shows the UK being ‘out of kilter’ with the level of regulation in the rest of Europe and other major insurance centres,” he said. “The costs that this extra regulation generates acts as a barrier to growth for UK brokers and may disincentivise new brokers from entering the market, thus impacting competition.”

The Biba-commissioned research, conducted by London Economics in 2014, found that UK brokers faced compliance costs that were approximately double that of the jurisdiction with the second-highest cost of regulation.

For larger brokers, the costs of compliance in the UK were more than 14 times the average across all other jurisdictions.

No comments yet