Commercial lines brokers cannot afford to have their heads in the sand thinking the incoming FCA general insurance pricing reform will only impact personal lines brokers

By Editor Katie Scott

The first deadline actioning the FCA’s general insurance pricing reform measures is fast approaching, yet a number of commercial lines brokers are “just not engaging” with the new rules and requirements, despite the fact that these regulations will “severely” impact their businesses.

This week, I listened in as Branko Bjelobaba, principal of general insurance compliance consultancy Branko, virtually addressed a collection of Leeds-based Chartered Insurance Institute (CII) members.

High on his agenda was emphasising the point that commercial lines brokers have until 30 September – around seven weeks away at time of writing – to get to grips with new product governance rules.

These are equally applicable to commercial lines professionals as they are to personal lines brokers dealing in motor and household insurance, which are the main target audience for the reform.

Bjelobaba said: “Myths – this only applies to motor and household. It does not. It really does apply to commercial. I’ve done several events and I’m actually concerned that lots of commercial insurance brokers are just not engaging.

“A lot of commercial insurance brokers have missed the fact that this applies to them. Some I’ve discussed [this] with think it’s just home and motor, but it is beyond that. If [brokers] do any commercial, this is severely going to affect [them].”

More than meets the eye

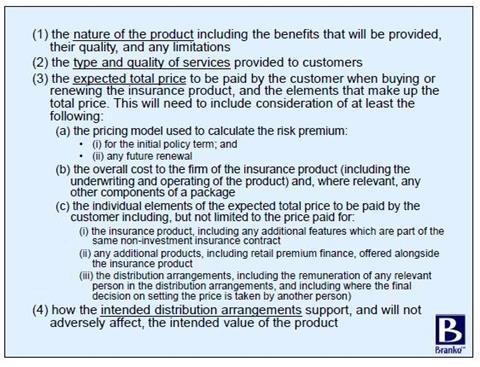

Offering more clarity on what exactly will impact commercial brokers from the FCA’s new measures, Bjelobaba continued: “The pricing and the premium finance rules do not apply to commercial insurance. The rules that apply to commercial insurance are the product governance rules. They deal with value, distribution, remuneration.

“The pricing rules do not apply to commercial, the premium finance rules do not apply to commercial per se – but then you are subject to other, more general rules where the FCA could say you are shafting your commercial customers by not offering them the cheapest form of premium finance, so you’re not acting in the customer’s best interest. That rule applies to all customers, not just personal lines.”

This product governance requirement, therefore, means that firms have to assess the value of their products at least every 12 months to ensure they are acting in their customers’ best interests. Although this will typically fall to the insurer to complete, brokers are still included in this rule’s scope if they have a hand in designing, developing, creating or underwriting the product. Even legacy products must be double checked, Bjelobaba added.

Distribution and remuneration arrangements also come under this product governance category – for example, intermediaries are required to review distribution arrangements, including remuneration, at least every 12 months to check that fair value is still being provided for customers across the entirety of the insurance supply chain.

Other nuggets that will impact on commercial brokers include:

- The value of the insurance product must be considered in terms of its entire lifecycle – so at inception and renewal. If fair value cannot be demonstrated, than the product must stop being marketed and distributed.

- Price optimisation practices may not offer fair value, for example auto-renewals or the use of premium finance. Vulnerable customers must also be fully considered.

Assessing fair value

As well as assessing fair value themselves, commercial brokers will also need to have an understanding of how insurers assess value – this includes having a broader understanding of the overall distribution strategy and how this may influence value.

“When it comes to commercial, it’s an assessment of the value,” Bjelobaba said.

In conversation with an attendee, Bjelobaba gave an example around residential property owners’ cover and the involvement of managing agents in the value chain – something brokers will now need to keep a weather eye on.

He said: “If that broker wants to split that [commission] down the middle with a property managing agent, that’s fine, they can do what they like with their money. That’s [the commission] you would have paid as an insurer.

“But if that broker is twisting your arm to push that [commission] up and you know that’s to accommodate someone else who is doing very, very little, that’s when that discussion needs to be aired and tabled in a grown-up manner to say that those practices are going to challenge what we do in this particular sector.”

Needless to say, this article merely skims the surface of the FCA scheduled changes – the policy statement published back in May was a tremendous 217 pages, while the new rules themselves amounted to 87 pages. Bjelobaba confessed it took him two full days to wade through this document.

The common thread, however, remains the focus on fair value – according to Bjelobaba, the word ‘value’ is mentioned more than 400 times across the rules.

Equally, the FCA plans to police its new rules carefully – last month, it even sent out a 50-question preparedness survey to poll firms’ readiness for the deadlines.

Insurance firms – including commercial brokers – simply cannot be caught on the back foot here considering the vast scale of the work to be completed. Although the headline of the reform is centred around price walking in the motor and home insurance markets, the ripple effects reach far and wide.

As Bjelobaba said, it’s time for both personal and commercial brokers to “smell the coffee”.

No comments yet