Broker ratings were boosted due to an uplift in complaints handling scores

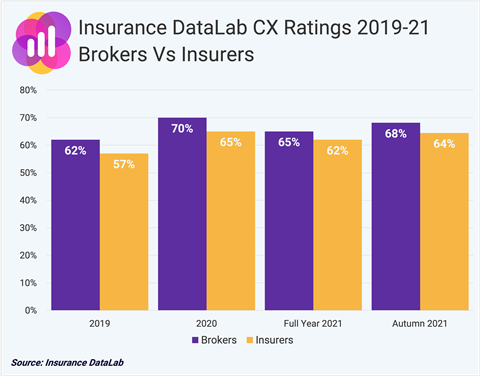

Brokers received a customer experience rating of 68% on average in autumn 2021, whereas insurers only scored a 64% customer experience rating, according to new research by intelligence service Insurance DataLab.

The research was based on Insurance DataLab’s own proprietary formula, devised for its inaugural Customer Experience Report, which was published in July 2021.

This provided a half-year update across 25 personal lines providers, exploring various metrics that cover the key elements of customer experience. This includes transparency, customer trust, happiness and satisfaction and complaints handling.

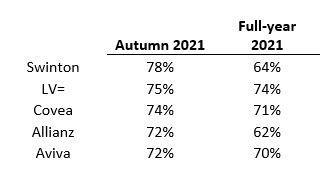

Insurance DataLab’s latest findings, published today (3 December 2021) show that broker Swinton has climbed to the top of its customer experience rankings, replacing LV= which fell to second place despite a one percentage point increase to its overall customer experience rating.

Overall, brokers improved their ratings by 12 percentage points on average, whereas insurers saw their average complaints handling rating climb by one percentage point over the last six months.

Brokers’ improvement here was fuelled by a 17% decrease in the volume of complaints about them that were referred to the Financial Ombudsman Service (FOS) during the second quarter of 2021, compared to a 6% decrease in complaints about the insurers included in Insurance DataLab’s analysis.

Overall, broker ratings were boosted by an uplift in complaints handling scores as the industry continues to bounce back from the adverse effects of the Covid-19 pandemic - the average broker rating for this metric is 63% for autumn 2021, compared to 60% for insurers.

The research also saw an improvement in the customer experience being offered by the UK’s leading personal lines insurance providers over the last six months.

Insurance DataLab’s co-founder Dan King said: “Our research shows that while improvements have been made in the last six months there is still much work to do, especially with the regulator expected to become more interventionist with the introduction of the fair value requirements.

“Both brokers and insurers will need to make sure that the services they offer are [commensurate] with the premiums they are charging and that they are not including unfair charges or policy exclusions that work to the detriment of the customer.”

Insurers gain customer trust

However, for research foundation Fairer Finance, insurers have come out on top - its ratings, using Insurance DataLab’s methodology - give insurers an average customer experience rating of 58% for autumn 2021, compared to 54% for brokers.

This represents a two percentage point improvement for insurers, up from 56% in the companies’ full-year rankings.

Brokers, meanwhile, saw their Fairer Finance rating fall by one percentage point over the same reporting period.

The companies in the analysis were rated highest for transparency in the pre-purchase journey, with brokers and insurers both receiving a 61% rating for this metric. This means that insurers increased their transparency rating by three percentage points over the last six months, while brokers remained steady at 61%.

The biggest difference in the scores between brokers and insurers came from Fairer Finance’s trust metric, with insurers outscoring brokers by an average of seven percentage points.

Under this trust metric, insurers received an average rating of 54% - up from 46% six months earlier. However, brokers saw their average rating for this metric fall to 47%, down from 49% in the full-year rankings.

Fairer Finance’s managing director James Daley said: “Personal lines insurers and brokers have enjoyed a good pandemic, with average happiness and trust levels rising significantly. But with the general insurance pricing measures coming into force next year, 2022 could prove a difficult year of transition for the industry.

“Many of the most active switchers will find that their prices increase - whilst many of those who benefit from lower prices may be oblivious. Insurers and brokers need to think carefully about how they communicate these changes to customers, so as not to give up the gains in trust they have made over recent years.”

No comments yet