Insurance DataLab provides exclusive analysis of the Financial Ombudsman Service’s most recent complaints data to see how prepared the industry is for the FCA’s Consumer Duty this July

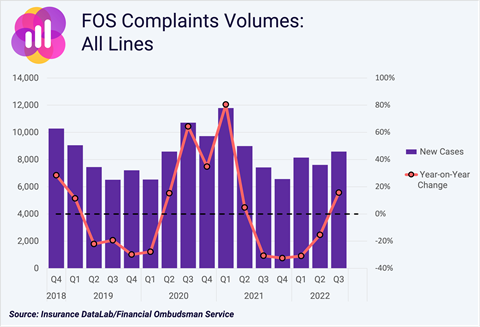

The volume of insurance complaints being referred to the Financial Ombudsman Service (FOS) is rising – now, complaints at the FOS are higher than the levels experienced immediately prior to the Covid-19 pandemic taking hold, according to the latest analysis from benchmarking platform Insurance DataLab.

A total of 8,584 complaints about insurance companies were referred to the FOS in the third quarter of 2022, which is 16% more than the same period a year earlier.

This figure is also almost a third higher than the 6,516 complaints referred to the ombudsman in Q3 2019 – the final third quarter results that were recorded before the impact of the Covid-19 pandemic hit the industry in early 2020.

Indeed, the most recent set of figures – from Q3 2022 – represent the busiest quarter for FOS referrals since Q2 2021, when almost 9,000 complaints reached the FOS after referrals peaked at 11,791 in the first quarter of that same year.

This trend will be worrying news for the insurance industry because the regulatory spotlight has arguably never shone as bright on the FCA’s desire for the financial services sector to deliver positive customer outcomes.

Intensifying regulatory spotlight

The FCA’s new Consumer Duty – set to come into force from July 2023 – specifically identifies complaints data as an area insurance companies should be focusing on in order to monitor customer outcomes.

This means that insurers, brokers and MGAs should all be keeping an eagle eye on their complaints data to see how they compare against market peers - this should also enable them to spot any problem areas where action may be needed.

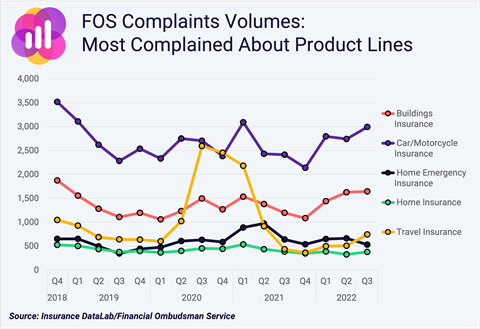

Car and motorcycle insurance may be a good line of business to start with here.

Insurance DataLab’s exclusive analysis found this class of insurance to be the most complained about insurance product over the last four years, accounting for around 31% of all complaints referred to the FOS.

The ombudsman received almost 55,000 motor insurance-related complaints over that four-year period, with referrals rising to 2,992 in Q3 2022 – up from 2,412 for the same period in 2021.

The second most complained about business line is buildings insurance, with almost 27,500 complaints being referred to the FOS over the last four years – this amounts to around 16% of all the insurance referrals reaching the ombudsman.

Travel insurance, meanwhile, is the third business line to make an unwanted appearance on the most complained about products podium – however, the 19,500 complaints referred to the FOS over the last four years was amplified by the impact of the Covid-19 pandemic.

Indeed, travel insurance-related complaints peaked at 2,594 in the third quarter of 2020 - at the height of the pandemic - before falling to 2,181 in the first quarter of 2021.

In the 12 months to the end of March 2021, 8,250 travel insurance complaints were referred to the ombudsman – amounting to more than 42% of all travel insurance complaints received by the FOS over the last four years.

Over that four-year reporting time frame, only five periods have seen travel insurance complaints exceed 1,000 referrals in a single quarter, with Q4 2018 being the only period to reach this figure despite not being affected by the impact of the Covid-19 pandemic.

If the Covid-impacted months are removed from the equation, then the average quarterly level of travel insurance-related complaints sitting with the FOS would have stood at less than 700 referrals.

Home emergency cover was the only other business line to have more than 10,000 complaints referred to the ombudsman over the last four years, with 12,337 complaints reaching the FOS.

Home contents insurance, meanwhile, was the fifth most complained about insurance product during the past four years, with approximately 8,400 complaints being passed to the FOS – around 5% of all referrals.

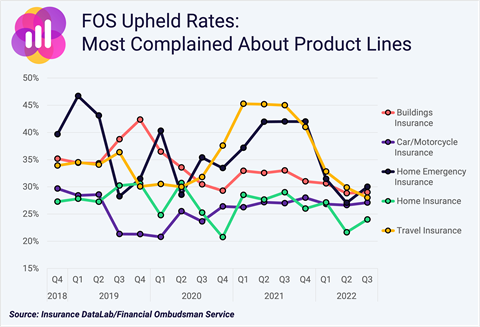

Upheld rates improving

But while the volume of complaints may be an interesting measure, the proportion of complaints upheld by the FOS in favour of the customer helps to give a more detailed insight into industry performance.

It is pleasing to see that over the last four years, the proportion of complaints upheld by the FOS in favour of the customer has been falling – with the exception of a spike in upheld rates during the Covid-19 pandemic – meaning that insurers are getting their decisions right more often than not compared to four years ago.

Of the five most complained about insurance products, home emergency cover has seen the most improvement, with the upheld rate for this business line falling by 12 percentage points over the last four years to 30%.

This is, however, still the highest FOS upheld rate of the five aforementioned products – ahead of buildings insurance (29%), travel insurance (28%), car and motorcycle insurance (27%) and travel insurance (24%).

Outside of these five most complained about products, there are some business lines that are bucking this trend and recording rising upheld rates.

Building warranty insurance has seen the biggest rise in the number of complaints being upheld by the FOS, with its upheld rate rising to 60% in Q3 2022 - up from 35% in Q3 2018.

This makes building warranty insurance comfortably the poorest performing product when it comes to the ombudsman finding in favour of the customer, with none of the other business lines having an upheld rate of 40% or higher in the third quarter of 2022.

It is worth noting, however, that the low volume of overall complaints about insurance products makes the upheld rate very volatile - with this figure has only exceeded 40% in five quarters over the last four years.

Mobile phone insurance, meanwhile, has seen its upheld rate rise by seven percentage points over the last four years to 34% in Q3 2022, while a 34% upheld rate for special event insurance in the third quarter of 2022 is one percentage point higher than the same period of 2018.

Valuing the customer view

Complaints handling is, of course, not the only measure highlighted by the FCA as area of focus for insurance companies - customer feedback is also cited as an example of where the industry can monitor its duty to consumers.

As part of this analysis, Insurance DataLab has reviewed data from research foundation Fairer Finance, which releases biannual customer experience scores for car, home and travel insurance each spring and autumn.

The good news here is that the average performance of insurance brands on this measure has been on the increase.

Car insurance leads the way with a Fairer Finance customer experience score of 66% as of autumn 2022 - up from 55% in spring 2018 - while home insurance has an improved customer experience score of 65%, compared to spring 2018’s 57% result.

Travel insurance, however, remains some way behind with a Fairer Finance customer experience score of 56% in autumn 2022 – just a four percentage point improvement on its spring 2018 score.

Technology is the key to improving

But while much of these metrics are moving in the right direction, there is still a lot of work the industry has to do.

With the vast majority of business lines having a FOS upheld rate of more than 25% – and all but three business lines having more than one in five complaints upheld in favour of the customer when reviewed by the ombudsman – it is clear that insurance companies are still not meeting customer expectations in many cases.

The expectation gap is one of the key drivers of this, with customers often not understanding the limits and exclusions that are built into policy wordings – they therefore expect their policies to protect them against risks that simply aren’t covered by their policy.

The impact of the Covid-19 pandemic on FOS complaint volumes and the subsequent spike in upheld rates also shows how the insurance industry is ill-equipped to deal with surge events and keeping customers happy in their times of greatest need.

The pandemic also demonstrated how certain products may have simply been inadequate – something the FCA’s fair value and Consumer Duty measures are both trying to address.

Technology can help in all of these instances, however, allowing insurers to simplify the quotation process while also enabling greater data gathering and enrichment. Embedded insurance could be a key tool here too.

Not only can technology help to close the expectation gap, but it can also create a slicker user journey, improving the overall customer experience.

Read: Complaints fall post-pandemic, but how is the industry really faring?

Read: MGA financials under the spotlight

Explore more news analysis here, or discover more financial stories here.

Automation and artificial intelligence are also becoming increasingly ingrained in clams processing.

Parametric insurance is seen as another way for the industry to improve the claims experience.

The speedy claims payments that are core to these products aims to create a much more user friendly experience – although this must be balanced with the fact that insureds are then responsible for processing their own repairs with the predetermined funds received.

So, while the new Consumer Duty and fair value regulations have undoubtedly increased the regulatory burden facing the insurance industry, they also present a great opportunity for the insurers, brokers and MGAs that are getting it right for end customers.

No comments yet