Businesses seeking trade credit insurance may find cover unavailable as insurers decline risks in this market at short notice

The ongoing burden of sanctions following Russia’s invasion of Ukraine in February 2022 has created significant issues for trade credit insurers, adding to the difficulties this market experienced during the Covid-19 pandemic.

For example, in early March 2022, many trade credit insurers pulled back from covering businesses that exported goods or services to Ukraine and Russia because of the risk of sanctions, potential claims and missed payments.

Trade credit insurance covers businesses in the event of a customer delaying payment or not paying at all for delivered products or services. Globally, this market underwrites around $3tr (£2.2tr) of trade receivables, according to trade body the International Credit Insurance and Surety Association.

Where some businesses have voluntarily chosen to withdraw operations from Russia as a result of the country instigating war with Ukraine, they are now faced with Russian counterparties deeming this pull back a ”breach of contract”, according to a statement from law firm Clyde and Co, published on 17 March 2022.

It noted that breach of contract accusations are especially rife regarding post-sale warranty and service obligations - however the question of whether these types of losses are covered under a trade credit insurance policy remains.

Mactavish’s chief technical officer, Rob Smart told Insurance Times: “The sudden removal of trade credit cover for some customers and suppliers can have a major impact on any company’s resilience, as they often are unaware that such cover is undermined by a war exclusion that becomes applicable in such circumstances [as the Russia-Ukraine conflict].”

Unlike most insurance policies, which are valid for a year or more, trade credit insurers can decline new business under a specific policy at short notice - leaving companies potentially scrambling to find suitable cover.

So, how is the Russia-Ukraine conflict impacting the trade credit insurance market and what is the potential fallout?

War exclusion

Trade credit insurance policies typically carry a war exclusion clause, meaning that policyholders cannot claim for war-related losses. This is common practice for the majority of commercial lines insurance policies.

Under this clause, policyholders cannot claim for war-related losses if there is a conflict between two of these five major powers: United States, Britain, France, China, or Russia.

Smart explained that due to the speed in which the removal of trade credit insurance cover happens, businesses can often find themselves unable to implement continuity plans, meaning they are unable to avoid using suppliers from certain countries or find new customers.

“Consequently, they find themselves suddenly uninsured, without notice at the moment the insurance carries real value for them. This [has been] exampled during the Russia-Ukraine crisis, [where] there is a risk of default and cover is withdrawn, Smart added.

“As a result, this often leads to widespread client scepticism around this class of insurance overall, as well as leading to uninsured losses.

”This scepticism massively limits the development of trade credit insurance generally and deters huge numbers of buyers away.”

Despite recent cover withdrawals, trade credit insurer Atradius reported that trade credit insurance was on the rise.

Within its 2021 financial results report, published in March 2022, the insurer noted a continued demand for trade credit cover due to ongoing uncertainty. However, the company did also pinpoint 2022 into 2023 as “another unpredictable year” because of insolvencies and political risks.

Read: Insurance sector rallies around Ukraine

Not subscribed? Become a subscriber and access our premium content

Downgrading ratings

In terms of the current war’s impact on insurers, credit ratings agency S&P Global Ratings predicted that the Russia-Ukraine war will add uncertainty, as well as exacerbate earnings volatility in global reinsurers’ specialty lines.

It added, however, that direct asset exposure is minimal.

In response to the conflict, Allianz Trade, formerly known as Euler Hermes, decided to downgrade its Russia risk rating from C3 to D4 - its highest risk ranking. Ukraine has been rated D4 since 2015.

The specialist trade credit insurer will also not be taking on any new or additional coverage for the Russia and Ukraine markets.

It noted that following recent sanctions - imposed by the UK government and European Union, among others - there has been a drastic drop in export volumes to Russian buyers from its policyholders.

As a result, Allianz Trade has adapted its exposure accordingly and plans to support customers that may still need to trade with affected regions, if permissible from a sanctions perspective.

In a statement, Allianz Trade said: “More than ever, we are committed to continue protecting our clients against all events which could impact their business and cashflow.

“We have been following the evolution of this conflict since the very start and have been very conservative in our risk positions and commercial underwriting stance in these markets for several years.

“Given the current context and the strong uncertainty about what will happen next, we have decided to take additional measures and adjust our underwriting strategy to the gravity and emergency of the situation.

“The situation is very closely monitored and we will adjust our actions further depending on the level of escalation of the attack and on the nature of the sanctions decided by the governments.”

Most exposed businesses

According to a December 2021 study conducted by the Federation of Small Businesses, which polled 1,271 small businesses, nearly one in ten respondents are facing insolvency because of late payments by clients.

Smart stressed that it is essential that businesses understand their whole supply and value chains, as well as identify and limit their dependencies, to manage and mitigate the impact of war-linked losses without relying on trade credit insurance.

He gave the example of a company having a client which may have lost some of its own onward clients or other key suppliers. The original company may might not have been wholly aware of its subsequent dependency on these firms.

Smart continued: “The most exposed companies are those smaller and mid-sized businesses with clients in affected areas where they continue to operate, such as essential goods categories.

“Businesses where the war has disrupted their clients’ financial viability indirectly have also been impacted.”

Nick Robson, global leader for credit specialties at broker Marsh, believes the lack of availability of trade credit insurance will impact businesses that export food, textiles and electronics to Ukraine and Russia, as well as companies providing products to the Ukrainian agriculture or Russian energy sectors.

PASS NOTES

How was the trade credit insurance market impacted during Covid-19?

The UK government introducted its Trade Credit Reinsurance Scheme (TCRS) in May 2020, to provide a reinsurance guarantee of up to £10bn for trade credit insurance during the Covid-19 pandemic.

The scheme was designed to help UK businesses continue to trade throughout the coronavirus pandemic, despite increased insolvency risks to supply chains, trade credit insurance being withdrawn and financial challenges caused by national lockdowns and pandemic restrictions.

The TCRS was effective between 1 April 2020 and 31 December 2020. It was later extended another six months, until June 2021.

How could Russia’s general insurance sector be impacted by the ongoing conflict?

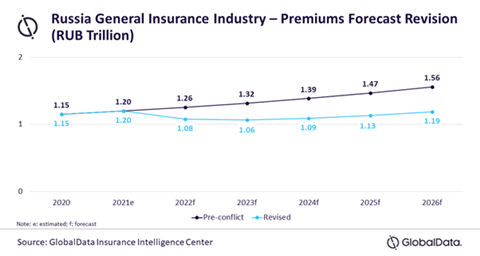

Russia’s general insurance (GI) industry is expected to decline by 14% in 2022 due to the ongoing war, according to figures published in March 2022 from analytics company GlobalData’s Global Insurance Database.

The short-term outlook for GI in Russia is bleak, the firm noted.

Deblina Mitra, senior insurance analyst at GlobalData, said: “Motor, property, trade credit and marine, aviation and transit insurance are expected to be among the most impacted [lines of business].

”However, increased risk volatility is expected to drive demand for political risks, war risks and cyber insurance products.”

No comments yet