Financial services consultancy says ‘the expectation for the industry to just pick up the tab for a once-in-a-century crisis like coronavirus is just not reasonable’

This year, the Covid-19 pandemic has had a transformative impact on the global economy – stock markets have tumbled in a downwards spiral since the beginning of the year and business sectors, such as leisure and entertainment, have effectively closed down due to a government-mandated lockdown, leading to furloughed employees as well as redundancies. The current uncertainty across industry sectors is palpable.

The insurance industry, however, finds itself between a rock and a hard place.

As well as facing the same fundamental financial fears that all businesses are encountering as the coronavirus outbreak continues, insurers and brokers are also inundated with claims enquires, due to travel restrictions or business closures for example. These firms are additionally tackling operational challenges, such as enabling staff to work securely from home, or attempting to manage the tsunami of phone calls flooding call centres. Reputational risk is a further concern as policyholders swiftly learn that policy wordings are not as inclusive as they imagined when it comes to covering the coronavirus fallout.

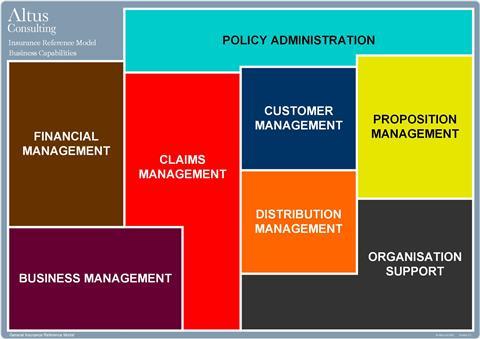

To aid these sector struggles, financial services consultancy Altus published a report in April which highlighted the key impacts of Covid-19 on business capabilities. The study, titled Impacts of Covid-19 on Insurance Businesses, further flagged recommended activities that insurers could implement to mitigate detrimental effects.

Speaking on the outlook for insurers in the present landscape, Mark Andrews, insurance director at Altus, said: “The insurance industry is getting a pretty rough deal at the moment. The expectation for the industry to just pick up the tab for a once-in-a-century crisis like this is just not reasonable.

“There have been calls from some for the industry to retrospectively change their policies to cover the pandemic. There are policies available that cover pandemics, as demonstrated by the LTA with Wimbledon and also the Tokyo Olympics. These insurance carriers will take a hit, but the claims will be paid. To suggest all business interruption should be retrospectively covered is simply wrong.

“Customers had the option to buy these policies and, perhaps more notably, brokers had the option to sell them.”

The key themes arising from the report that affects numerous business capabilities of insurers includes communications with customers and brokers, the likely growth in customer vulnerability, working towards greater operational resilience in the short and longer term, as well as how overall challenges have been magnified by the legacy nature of existing technology and contact centre models.

Claims

Although both travel and business interruption claims have skyrocketed due to coronavirus, a key concern within the claims sector is the timing of the Covid-19 outbreak – hot on the heels of storm and flood damage earlier in the year, Patrick Hayward, consultant at Altus, said this is therefore having a compounding effect on claims.

“The reality is we’re still coming to the tail end of the recent storm events earlier in the year; there’s a compounding impact of trying to manage those claims whilst dealing with another significant influx, whilst also trying to move a significant proportion of your workforce to working from home and that in itself, just getting the devices and setting it up, is all going to add potential friction to that process,” he said.

“Insurers are going to need to try to identify how they can manage the capability across their business and that potentially means looking at being flexible about who’s managing your notification processes.

“You might be looking at where there’s a reduction in the number of motor claims coming in, there’s reduced levels of road activity and it might mean that you’re flexing your FNOL teams, to involve people working in motor moving across to travel and so on.”

Steve Whitfield, senior consultant at Altus, added that “there are some real challenges to claims at the moment”. This includes the loss adjusting process, as staff are unable to access policyholders’ homes, and also the potential for increased levels of fraud.

“The balance of managing fraud in times like this where, undoubtedly, delegated authority limits will be increased and small claims are likely to be paid with not necessarily the same level of investigation that you may have in quieter times as well,” he continued.

The clarity of policy wordings is also important within the coronavirus claims minefield, especially considering the constant confusion surrounding business interruption triggers.

Hayward added: “There will be a need to remove any potential ambiguity in this area because although [this] is a very low frequency event, when it does occur, if there are challenges around policy which mean that claims do need to be paid where [that] wasn’t intended, it could be quite substantial from an industry perspective. It will definitely mean a tightening of policy wordings but also maybe a greater demand for this kind of cover in the future as well.”

Vulnerable customers

However, for Whitfield, the most striking coronavirus-related impact to emerge from Altus’s report centres around the treatment and consideration of vulnerable customers.

“This particular position that we find ourselves in, we will see a massive increase in customers who are vulnerable for various different reasons, be that that they are ill, or they [have a] loss of income, [or a] change of circumstances, which will lead them to be vulnerable for a temporary period of time,” he said.

With these new types of vulnerability affecting a myriad of different customers, Whitfield added that insurers need to evaluate how mature their vulnerability assessments are as well as ensure that those considered to be vulnerable can access suitable aid quickly and efficiently, for example enabling furloughed staff to take payment holidays while they are on a reduced income.

“The thing that some insurers potentially find difficult to get their head around is that vulnerability isn’t a permanent position,” Whitfield continued.

“It’s not you are vulnerable, or you are not vulnerable. It can be, especially in times like now, a temporary position, so it’s not an assessment of your customer base to say ‘are they vulnerable, yes or no’. It’s being able to train your front-line staff to be able to recognise signs of vulnerability. It’s then being able to put processes and treatment strategies in place to ensure that you are treating those vulnerable customers fairly, and I think that’s the challenge.”

Whitfield recommended that insurers engage with brokers to support vulnerable customers, especially at times like renewals. Short extensions in cover, for example, allows all parties more time to explore relevant questions and also provides flexibility for vulnerable customers to make a clear decision about their cover, especially if their circumstances have changed.

Alongside payment holidays, insurers could additionally suspend processes that lead to automatic termination of cover – again mitigating the extra time communication can take because of insurance staff working remotely. Firms can also relax conditions that are difficult to adhere to because of the Covid-19 outbreak; the industry’s decision to relax requirements around MOT certificates, in line with legislative changes to allow for this, is a good example here.

Effective proposition management

Financial services consultancy firm Altus believes that proposition management is one of the business capabilities that will be impacted by coronavirus. Not only will pricing be affecting, but also the risk appetites of customers.

Its recent report read: “We are likely to see changes in customer behaviours linked to the pandemic event and altered perceptions of risk, which will impact the nature of the insurance cover they seek and most likely increase the extent to which they want to be covered.”

To tackle potential issues in this area, Altus recommended:

- Review policy wordings to determine whether there are changes that should be made to reflect a better understanding of the potential risk for pandemics, to address the fluctuating position we may see in the next six to 18 months and increased demand for cover from businesses.

- Revise underwriting manuals and update system rules where necessary – changes will need to be assessed for customer and downstream business impacts.

- Proactively communicate with customers and review existing campaigns to ensure consistency of message, and potentially to avoid inbound volume increases.

- Update propositions – whilst insurers are making changes to policies in response to the current situation, there may be a move to updating existing propositions so that they clearly support the activities of key workers and some types of voluntary activity.

No comments yet