The extent of the cashflow challenge facing Ardonagh is revealed today in an Insurance Times financial analysis

Ardonagh is confident it can manage its liquidity - but it is going through cash at a rapid rate (see graph).

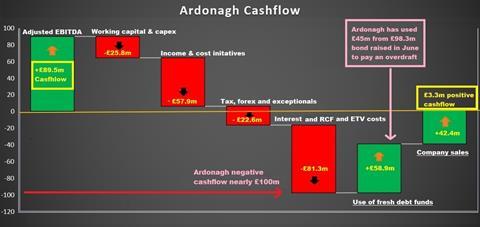

The consolidator made just £3.3m in cash this year, latest results show.

And to achieve that result, Ardonagh had to tap the bond markets in June for more money and use £42.4m banked from the sale of companies.

Without these additions, the consolidator would have ended up nearly £100m in negative cashflow.

Credit facility demand

One of the demands on Ardonagh has been paying back a £45m revolving credit facility - the RCF - which is effectively a form of overdraft.

To pay off the RCF, Ardonagh has used nearly half of the £98.3m bond - which has an 8.37% interest demand - raised in June.

The rest will be used for investing in the business.

Cashflow was the issue which caused the Mark Hodges-led Towergate to nearly collapse in 2014 and heralded the arrival of David Ross following a debt restructure and financial rescue.

Ardonagh boss David Ross: Investing heavily for the future, but it is putting a strain on cashflow

Ardonagh says management of liquidity is a ‘key priority’ for the group.

The insurance group has this year improved forecasting capability to spot any liquidity constraints.

“Management is confident that the group will be able to meet expected cash outflows and debt covenant requirements while maintaining a liquidity buffer to manage any volatility in terms of timing and amounts,” the third-quarter financial statement said.

Short-term funding gaps will be plugged by the £120m RCF.

Meanwhile, liquidity has been improved by the £235m bond issued last month. Most of the bond was used to buy Swinton for £165m.

Ardonagh has also cleared the interest payments on its bonds for the year, giving it better chance of improving cashflow by the year end.

Costly investment, long-term benefit

The consolidator is getting to grips with a number of costly issues, which are taking its toll on cashflow.

The very things that management say will strengthen the business long-term - the costs of the business transformation, capital expenditure, transformational hires, M&A investments - also weaken cashflow in the short-term.

Add the interest on debt, plus the consistently expensive one-off costs, and it’s the reason why Ardonagh - despite having essentially profitable businesses across the SME, corporate and protection markets - can barely muster any cash.

The key question market commentators are now asking themselves is whether the Ardonagh management can battle through these headwinds and fulfil their long-term aim of having a high-earnings insurance business, throwing off healthy cashflow.

Ardonagh is 80% owned by private equity firms MDP and HPS. LA Fitness is owned by MDP.

Ardonagh has £1bn debts to repay by 2023.

A credit report last month from highly-respected analysts at Debtwire lays out the issues.

It states: ”Ardonagh faces significant execution risk given multiple recent acquisitions, underperformance of the MGA business, high leverage, and weak FCF (free cash flow) generation due to persistent one-off costs, high growth capex and high cash interest expense.”

On the upside, it is recognised by both Moody’s and Debtwire that Ardonagh could save nearly £40m a year and end up with a much improved, cleaned up business, if it can see through its strategic plans successfully.

The strategic plans include things such as consolidating the IT onto one platform, the cost savings, investments in transformational hires and M&A.

Debtwire states: ”Noteholders could see upside if the operating performance sustainably improves after a successful execution of the transformation plan and restructuring.

”Ardonagh is well-diversified with product offerings that cover most segments of the insurance market including niche products for corporate, retail and SME clients.”

Moody’s says the execution risk is ‘limited’, although the magnitude of expected revenue and profitability remains uncertain.

“Moody’s expects run-rate savings (approximately GBP40 million in 2018) to materialise over the next couple of years and exceptional costs to come down. As this happens, the group will be in a strong position to grow its statutory earnings and start generating organic positive net cash flows,” the rating agency says.

Debtwire believes ‘execution risk is high’.

”There are a lot of moving parts given the multiple acquisitions and an aggressive cost reduction and synergies target,” it concludes.

No comments yet