The ‘largest threat to insurers’ following the pricing rule change ’is likely to be from pay-per-mile motor insurers’, says insurance analyst

The FCA’s general insurance pricing reform has restricted UK consumers from switching to different insurers at renewal for a lower premium, according to data and analytics firm GlobalData.

The pricing reform fully came into effect on 1 January 2022 - it aims to protect consumers by abolishing price walking, preventing insurers from offering cheaper policies to new customers while increasing prices for existing policyholders.

However, GlobalData believes that a lack of preferential rates will make it harder for consumers to shop around for cheaper premiums.

The data and analytics company therefore suggested that the FCA and insurers will need to work together to ensure that premiums do not continue to rise sharply throughout 2022, especially as UK consumers are now facing low wage growth and an increased cost of living.

GlobalData insurance analyst Ben Carey-Evans said: “As motor is a compulsory line, there is not a great deal that consumers can do and insurers do not face the risk of people cancelling policies, as in other lines.

“Rising prices will undoubtedly lead to more shopping around at renewal, but if no leading insurers are offering competitive premiums to new customers, then the [number] of consumers switching will not necessarily rise.”

Premium patterns

So far this year, motor insurance premiums have jumped more than £100, according to The Mirror (4 January 2022).

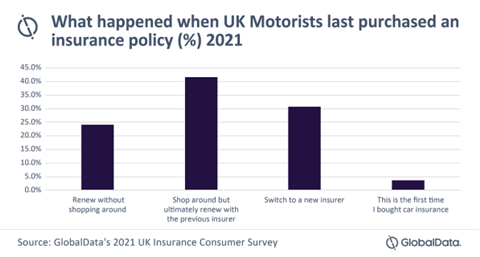

GlobalData’s 2021 UK Insurance Consumer Survey - which was published in Q4 2021 and received 4,000 responses - further found that 77.8% of motor insurance customers switch at renewal because a different insurer offered a lower premium.

Just under a third (30.7%) of all consumers polled switched to a new motor insurer in 2021. Another 41.6% of respondents shopped around for motor cover, but ended up staying with the same insurer.

Carey-Evans added: “The largest threat to insurers is likely to be from pay-per-mile motor insurers.

“These are generally startups, with companies such as Metromile and By Miles leading the way.

“Their policies offer consumers a cheap basic rate for the year and then they will pay a flexible rate based on how much they drive.

“This means they can control costs and it may even be more fitting anyway, with fewer consumers commuting to work on a daily basis due to Covid-19.”

No comments yet