James Burton Director of Product Management at LexisNexis Risk Solutions speaks to Insurance Times on the value of data enrichment and the perceptions of personal motor insurers on the current and future benefits of contributory databases.

What were the aims & objectives of the study?

We wanted to explore Personal Motor insurers’ perceptions of the current and future benefits of contributory databases – whether that be improved profitability by making better decisions faster or being able to improve fraud detection through unique insights. This was part of a much wider research study seeking industry views on defining digital strategy and digital risks, to understanding the value of using data enrichment.

Regular industry research such as this is part of our commitment to delivering data and technology solutions to help insurance providers make more informed decisions throughout the customer lifecycle.

What were the stand-out findings from the study?

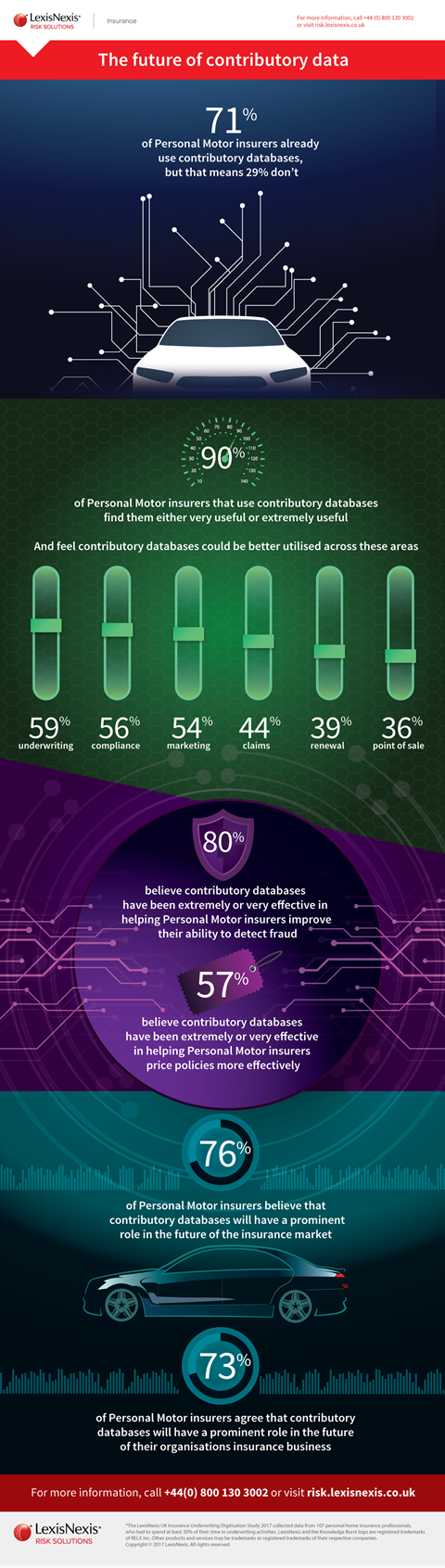

Almost a quarter of a century since the first contributory database entered the insurance industry, the study revealed that, 71% of personal motor insurers are using some form of ‘shared’ data such as No Claims Discount information and claims history at point of quote and point of underwriting.

It was clear from our study that most motor insurers find contributory databases very useful and a majority feel they could be even better utilised for underwriting (in 59% of cases), compliance (56%), marketing (54%) and claims (44%). Furthermore 76% felt they would have a prominent role to play in the future of motor insurance markets, which to us demonstrates the value and insights the majority of the market see from this type of data enrichment.

In the study, 57% felt contributory databases have been extremely or very effective in helping personal motor insurers price policies more effectively, why do you think this falls below the response for their ability to detect fraud with 80% of insurers ranking them as effectively detecting fraud?

Our survey asked insurers to rank the effectiveness of contributory databases in achieving their organisational goals. One of the primary reasons motor insurers use contributory databases is to help detect and combat fraud – 64% stated that this is one of their main aims, followed by more accurate pricing (54%), operational cost saving (49%) and better risk assessment (41%). So when we asked the same insurers how effective contributory databases are in helping them achieve these goals, 80% of insurers ranked them as being extremely or very effective in their ability to detect fraud while 57% ranked them highly for pricing policies more effectively.

This really underlines the focus the motor insurance sector is putting on combatting fraud given the challenges facing this corner of the market. However, we are seeing a shift in the motor insurance market place with greater emphasis placed on improving the customer experience in order to aid better retention rates, including that of more accurate, personalised pricing. We expect that as the market changes and evolves towards more digitised workflows, that contributory databases will have a bigger part to play in improving policy pricing accuracy on top of the benefit already seen with fraud identification.

For the proportion of respondents who stated it had not helped them price policies more effectively, why do you believe this to be the case?

There are several possible reasons for this – the biggest barrier we believe for some is that it has not yet been tried and tested. It might simply be a scenario of ‘you don’t know until you’ve tried it’ when appreciating the benefits of contributory databases. The other factor is possibly the inclination of larger insurers to protect their data sources and loss models combined with a misconception that sharing information could be a loss of competitive advantage. These concerns are unfounded. Contributory databases can actually improve competitive advantage. Keeping data locked within one company is limiting – most insurers agree that it makes sense to collaborate and combine data into one comprehensive information pool.

In essence, contributory databases offer the best of all worlds and the vast majority of motor insurers are recognising this point. 59% of motor insurers in the study believe that contributory databases will benefit underwriting and claims, 39% say renewal and 56% compliance.

Large insurers are increasingly investing heavily in their own extensive analytics capabilities, will this lead to an increase or reduction in sharing data via contributory databases?

Whatever the size of an insurance provider, operating in a silo can create blind spots and security gaps, leading to inaccurate risk profiling, inaccurate pricing and potential losses through claims and fraud.

No single insurance provider can ever gain an industry-wide view that is achievable through contributory databases. This applies to even the largest insurers, who may have a market share of 10-15%, thus leaving a large proportion of the market data under-analysed.

Aggregated information from across the insurance market fills in the missing gaps of information. It can confirm details provided by an applicant or claimant, mitigating risk from incorrect information or accidental miss-states and providing a far more detailed picture of that customer, their risk, their propensity to cancel, claim and any indicators of fraud. Contributory databases provide a source of information that is otherwise not obtainable.

Therefore, larger insurers will not lose their pricing advantage. It’s a virtuous cycle for all involved. Contributory databases are also key in automating and simplifying workflow. They help the insurance industry enrich existing data, without damaging an individual insurer’s competitive advantage. They help to drive efficiency with an ability to participate in product innovation without impacting internal IT resources.

Is there a risk of model building without seeking the right permission if the insurer in question holds far more advanced analytics capabilities?

There are various data protection constraints around how personally identifiable data is pooled and for what intended uses, therefore any advantages sought in this regard are legislated. For example no pooled insurance data obtained and held by anyone operating within the insurance industry under one permitted purpose agreed with the data subject, such as for underwriting purposes, can then be used for another intended purpose, including model building and internal analysis, without ensuring the right express permissions for that use are obtained first.

Many in your study felt contributory databases should work harder in areas such as underwriting and compliance, how in your opinion can this be done?

It’s simple, contributory data needs to be injected at point of quote to provide a deeper understanding of the customer, smooth the customer journey and reduce instances of miss-states and mistakes for example in respect of NCD declarations or previous cancellation history. This allows for more informed underwriting and the delivery of fairer more personalised pricing to the customer, reflecting their individual risk, and in a fully compliant manner.

This type of individual risk assessment using prior insurance policy based information rather than just public records information, supports more accurate pricing and underwriting processes, and risk mitigation in the first instance, avoiding insurer led cancellations and ensuring compliance. At the crux of the issue is integrating the data as part of an insurer’s quote workflow, which is possible through platforms such as Informed Quotes from LexisNexis Risk Solutions.

An individual company may have an edge on competitors by having advanced analytics and data, why would they share the data for the greater good when they may feel it keeps them ahead of competitors?

Competition between insurers will always be part of doing business. The perceived fears around losing the competitive edge by using contributory databases are exactly that – purely perceptions. When we put the question of competition to the study respondents, the results were quite surprising.

The majority (86%) of motor insurers said that contributory database insights will make the motor insurance industry at least somewhat more competitive. 13% have the view that this will lead to a high degree of competitiveness overall in the future. What we do know is that the participants in contributory databases receive a boost to their competitive advantage, while the non-participants do not.

With contributory data, we are essentially talking about new, unique risk insights and attributes from ever-greater granularity of risk. No matter what type of insurer you are, you cannot fail to benefit when you have additional risk insights, and more customers to quote on.

From the consumer’s point of view, if insurers have more accurate information to better assess risk at an individual level, it will free them up to focus their competitive advantage on creating an improved customer experience, strengthening brand loyalty and improving post-sales service. This is key in the move towards more personalised services demanded by today’s consumers. So contributory databases are not just about bottom line loss ratios, there’s a real benefit to the consumer too.

What action would you like to see occur with contributory databases in the year ahead?

As the volume of data continues to grow, the potential increases for more accurate, personalised pricing and rewards to help incentivise better behaviours and reduce risk. As the additional data points begin to feed into the data pools already existing, a more detailed picture of customers, applicants and the market generally will emerge and the power of contributory databases will only grow. With such clear advantages and no disadvantages, we believe it will not be long before the 71% of motor insurers using contributory databases, becomes 100%, and that it’s usage from being a predominantly underwriting based benefit will be seen across other areas of the insurance workflow.

In January 2017, LexisNexis Risk Solutions released a comprehensive study on how digitisation is affecting the UK insurance market today. Conducted anonymously, the survey included a variety of insurer perceptions, attitudes and market insights – from defining digital strategy and digital risks, to understanding the value of using data enrichment and contributory databases.

Using a mix of online panel and telephone interviews, we collected data from 107 insurance professionals, who all answered questions specific to their insurance line. To take part in the survey they had to spend at least 30% of their time in underwriting-related activities. The results showed that the majority of respondents spent over 80% of their time pricing and underwriting policies. LexisNexis was not identified as the sponsor of the study (conducted 8th December - 9th January 2017).

Hosted by comedian and actor Tom Allen, 34 Gold, 23 Silver and 22 Bronze awards were handed out across an amazing 34 categories recognising brilliance and innovation right across the breadth of UK general insurance.

No comments yet