The UK motor insurance market has faced some tricky times of late, and although the Covid-19 may provide some temporary relief from rising claims costs, research from Deloitte predicts additional road works down the line that will put further pressure on already strained net combined ratios

Ogden, technology, regulation, Brexit and now the Covid-19 pandemic. The UK motor insurance market has had much to contend with.

Looking back, the market did not make underwriting profits between 1995 and 2016 when net combined ratios exceeded 100% every year. But for the first time in more than 25 years, 2017 and 2018 saw the market return to underwriting profitability following the adverse impact of the Ogden discount rate change in 2016. However, in 2019, the market’s underwriting performance dipped into unprofitable territory once again, delivering a 100.8% net combined ratio.

However looking ahead to the short- to medium-term, the likes of Brexit, regulation, the competitive landscape, sustainability and technology are all expected to continue to place further pressure on underwriting performance.

Although Covid-19 introduces uncertainty for future performance, reduced levels of mobility are expected to have a positive impact on motor insurers’ profitability. To understand this uncertainty, we have analysed the main interrelated drivers of future performance: the economy, mobility trends and shifting consumer behaviour.

Economic impacts

Our Economics team forecasts, in the latest Deloitte Economics Monitor, a 12% contraction in UK GDP in 2020. This would be the sharpest annual decline in more than a century and far greater than the 4% drop in 2009, at the height of the Global Financial Crisis.

The team expects a partial recovery next year, with GDP forecast to rise by 9% in 2021.

Historically, motor insurers have seen combined ratios deteriorate during economic downturn – largely driven by reduced consumer spending – which leads to suppressed levels of car sales and therefore reduced demand for insurance products. But they can also be impacted by reduced average premiums where, due to financial constraints, customers opt for the minimum level of cover required rather than purchasing more expensive comprehensive covers and additional benefits.

Also, claims costs can rise as a result of higher levels of fraudulent claims and repair cost inflation due to economic factors.

In Q2 2020, SMMT revealed that new and used car sales were down 67% and 25% respectively compared to Q1 2020. This is mainly due to fleet sales, which account for around 55% of new car sales, being wiped out over the last three months.

This has been exacerbated by the closure of showrooms over lockdown as well as financial pressure on households. Further research from Deloitte anticipates that total car sales are unlikely to reach pre-pandemic figures again until 2024.

Mobility trends

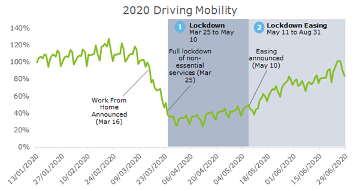

During lockdown, UK mobility dropped by more than 90% of typical levels and driving levels dropped by 75%, as illustrated by the graph below.

However, since lockdown easing began on 11 May 2020, mobility levels have started reverting towards pre-lockdown levels.

As the UK government lifts further restrictions, we expect driving levels to increase, but we do not expect pre-lockdown levels to return by the end of 2020 due to changes in consumer behaviour.

Changes in consumer behaviour

The Covid-19 pandemic has significantly changed why and how we travel, which is expected to redefine the future of mobility.

Data from the Department for Transport shows that on average, of the miles driven in the UK per person per-year, 42% were for leisure purposes, 28% for shopping and personal admin, 26% for commuting to work and 4% for education.

Given the continued public nervousness and the desire to maintain social distancing, we are expecting individuals to travel less – particularly by public transport – as well as change their reason for using motor vehicles.

For example, more employees will continue to work from home and more people will continue to opt for online retail, as visits to physical shops remain less attractive. Furthermore, we anticipate increased driving for leisure purposes with restrictions on international travel, as well as personal financial constraints.

In aggregate, we forecast a 20% decline in annual distance travelled by car for 2020 relative to 2019. This is resulting from a decline in total mobility, overlaid with changes in reasons for travel and changes in modes of transport, followed by a 15% increase in 2021 relative to 2020.

Based on our research conducted on providers’ Solvency and Financial Condition Reports, expectations for future mobility trends, consumer behaviour and economic outlooks, we estimate the UK motor insurance market’s net combined ratio performance to improve to 94.1% in 2020. However we expect it to deteriorate to 105.6% in 2021.

Overall, we expect 2020 to be a record year for UK motor insurance market underwriting results. This result is primarily driven by claims cost reductions following significantly reduced levels of motor vehicle accidents.

Looking further forward to 2021, however, we expect to see Brexit-related inflationary pressure on claims costs and competitive pressures on average premium levels to result in a return to underwriting losses with a net combined ratio in the range 102% to 111%. This of course will be highly dependent on the extent of economic recovery, the shift towards the new normal of mobility and consumers’ driving habits and providers’ pricing actions.

With the expected profits in 2020 not being sustained next year, insurers continue to face challenges around underwriting profitability. With changing customer behaviour, data, digitalisation and technology easier to access and leverage now more than ever, it is time for insurers to embrace change and refresh their offering.

Read more…

No comments yet