Insurance DataLab unpicks the latest complaints data from the FOS to highlight the direction of travel for insurance service

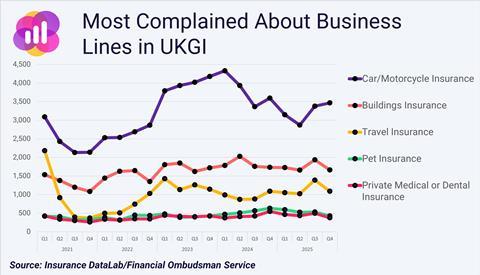

Motor insurance continues to be the most complained-about business line in UKGI, according to the latest analysis of Financial Ombudsman Service (FOS) complaints data by market intelligence firm Insurance DataLab, published exclusively by Insurance Times.

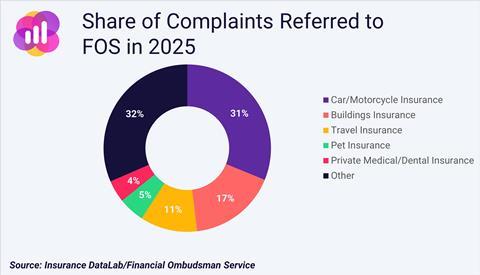

This analysis reveals that the FOS received a total of 12,860 motor related complaints over the course of 2025 – equal to almost a third (32%) of all cases referred to the ombudsman last year.

This is, however, a year-on-year drop of 15.5% compared with 2024 - suggesting that recent years’ surge in motor cover complaints, driven in part by claims inflation, repair delays and wider supply chain disruption, may now be beginning to ease.

Motor insurance complaint volumes have now fallen in five of the last six quarters following a surge of complaints in 2023, when complaints rose to an annual peak of a little under 16,000.

Motor insurers also reported an improved upheld rate for 2025, with the FOS finding in favour of the customer in 36.5% of cases in 2025, compared to 43% in 2024.

Insurance DataLab co-founder Dan King noted that the FOS data indicated a turning tide in motor insurance complaints.

“Motor will always dominate the complaints data simply because of its scale, but the recent fall in both volumes and upheld rates suggests the market is beginning to regain some operational control,” he said.

“After the disruption of the past few years, there are early signs that improvements in claims oversight and customer handling are starting to feed through.

“The challenge now is maintaining that progress in what remains a complex and high pressure line of business.”

Complaints volumes

The second most complained about business line is buildings insurance, with 6,982 complaints referred to the FOS in 2025, down from 7,304 in 2024. This is an annual reduction of 4.4% – although the business line still accounts for more than 17% of all FOS complaints.

Read: FOS complaint levels climbing despite Consumer Duty reforms

Read: Latest FCA complaints data reveals drop in motor-related disputes

Explore more Data Matters content here, or discover other news analysis stories here

Meanwhile, third on the list is travel insurance, with 4,553 complaints with the FOS in 2025. This is an increase of 18.9% on the 3,828 cases reaching the ombudsman in 2024, making travel insurance one of just two products in the most complained about business lines to report growing complaint volumes last year.

Indeed, the 18.9% increase in travel complaints is the second highest increase across all business lines – contrasting jewellery insurance, which received just 23 complaints in 2025.

This rise in travel complaints comes amid heightened scrutiny of customer outcomes across the sector following last September’s Which? super-complaint to the FCA.

The consumer group argued that both travel and home insurance markets were delivering “systemically poor outcomes”, particularly when customers attempted to make a claim.

Which? cited concerns around claims decisions, policy wordings and the way some insurers handle disputes with policyholders.

While the FCA has acknowledged the concerns raised in the super-complaint, it stopped short of launching a full market investigation. Instead, the regulator said it would assess the issues raised via its existing supervisory work and ongoing monitoring of insurers’ compliance with Consumer Duty rules, which were introduced in July 2023.

King said that the super-complaint represents a further escalation in the debate around claims handling and customer outcomes.

“The Which? super-complaint has intensified scrutiny on how insurers handle claims and communicate policy coverage, particularly in travel,” he explained.

“When a consumer group escalates concerns to that level, it inevitably sharpens regulatory and public attention on customer outcomes.

“For insurers, it’s a reminder that clarity of wording and consistency in claims decisions are just as important as price or distribution.”

Concentrated lines

Pet insurance has also attracted significant attention regarding customer complaints, with rising veterinary costs and increasingly complex policy structures often cited as contributing factors behind disputes in the market. However, FOS complaints turned a corner by falling 4.5% to 2,072 in 2025, after peaking at 2,169 the previous year.

Indeed, the final quarter of 2025 experienced a 33% drop in complaint volumes – the biggest year-on-year decrease of the last five years – with the pet insurance market benefitting from two consecutive quarters of falling volumes.

Despite this, pet insurance complaints have the second highest upheld rate across the UKGI marketplace at 45% – just 0.5 percentage points behind the worst offending business line, commercial property insurance.

Rounding off the list of the most complained about business lines in UKGI is private medical and dental insurance with 1,770 cases referred to the FOS in 2025, up from 1,750 over the course of 2024.

This business line’s upheld rate, however, is considerably better than the products at the top end of the complaints league table, with just 23% of cases found in favour of the customer in 2025.

This is the third lowest upheld rate in the whole of UKGI, just behind personal accident insurance (22.9%) and commercial legal expenses (20.7%).

Taken together, the five most complained about business lines account for close to 70% of all insurance linked disputes reaching the ombudsman, highlighting how complaints in the UKGI market remain heavily concentrated in a small number of high-volume personal lines products.

But while complaint volumes vary significantly between business lines, the nature of those complaints is far more consistent across the UKGI market.

Claims focus

Analysis of the latest FOS data shows that the overwhelming majority of the disputes referred continue to relate to the claims process. Across all general insurance business lines, claims related complaints accounted for 26,430 cases in 2025 – comfortably the largest category of dispute.

Administrative issues represent the next largest source of complaints. These cases – which include issues such as poor customer service, disputed charges and issues around mid-term adjustments – accounted for around 8,400 referrals to the FOS last year.

By comparison, complaints relating to sales or advice remain far less common, with just over 2,500 cases recorded across UKGI in 2025.

Taken together, this means that claims disputes account for roughly seven in every ten complaints escalated to the ombudsman.

This pattern is consistent across most major product lines, with disputes typically arising when customers disagree with either the outcome of a claim or the way that a claim has been handled.

Promises kept?

Indeed, this concentration of complaints around claims decisions reflects the point at which policyholders most directly test the promises made in their insurance policies.

And King argued that, when customer expectations are not met, complaints inevitably follow.

“Insurance is ultimately tested at the point of claim and that is where expectations and reality often collide,” he explained.

“When the outcome or the process doesn’t align with what a policyholder believed they had bought, complaints are almost inevitable.

“But the lesson in the data is clear – strong claims handling and clear communication remain the biggest determinants of customer trust.”

Despite this finding, across the most complained about business lines all but pet insurance recorded improved upheld rates for claims complaints in 2025, suggesting that insurers were more frequently able to demonstrate that claims decisions had been applied in line with policy terms.

Taken together, the figures reinforce the central role that claims handling continues to play in shaping customer outcomes across the insurance market.

While complaint volumes may fluctuate across different products from year to year, the underlying driver remains largely the same – how clearly policies are written, how consistently claims decisions are applied and how effectively insurers communicate outcomes to customers when disputes arise.

No comments yet