Law firm reveals litigation around BI claims is still on the table for this year, especially as the FOS appears to be siding with insurers in the majority of BI-linked cases since last January

By Editor Katie Scott

It’s now been a year since the Supreme Court issued its verdict on the FCA’s business interruption (BI) test case appeal and although BI claims stories are no longer hitting headlines with frequent fervour, these claims are still very much rumbling along in the background – as evidenced by the monthly data the FCA publishes on its website.

However, for policyholders who are unhappy with their claim result, the affordable and seemingly simple recourse offered by the Financial Ombudsman Service (FOS) has not been all it’s cracked up to be, according to law firm Weightmans.

In a webinar this week in conjunction with the Insurance Institute of London, Weightmans associate Pamela Freeland explained that when searching the FOS’ published decisions for BI claims disagreements that were investigated after the Supreme Court judgment last January, only two out of 211 decisions decreed that the coverage decision was wrong to find in favour of the policyholder.

The majority of FOS decisions, it appears, align with insurers, contradicting the perception that many within the industry have of the FOS’ role in the BI debate. When speaking to insurance commentators over the course of the pandemic, many signposted the FOS to me as the first port of call struggling SME policyholders should look to.

Freeland identified a few trends across the published FOS decisions, indicating its reasoning. Firstly, that Covid-19 does not cause property damage or a physical loss – even if the virus is found to be at the premises, it does not alter the physical state of the property, she noted.

This issue was not addressed in the test case, Freeland added.

The FOS also typically agreed with insurers in cases where a closed list of diseases is included in the policy wordings, confirming which illnesses are covered. The ombudsman felt this clearly demonstrated the insurer’s intention and that less restrictive policies were available if policyholders didn’t agree with the closed list T&Cs.

It added that Covid-19 could not be classified as SARS or plague either.

Other cases discussed the manifestation of an infectious disease at the insured property and whether this caused business closure. The FOS, however, primarily identified the UK government’s orders as the reason for shutting up shop, meaning cover would not available under disease clauses.

Tackling the claims backlog

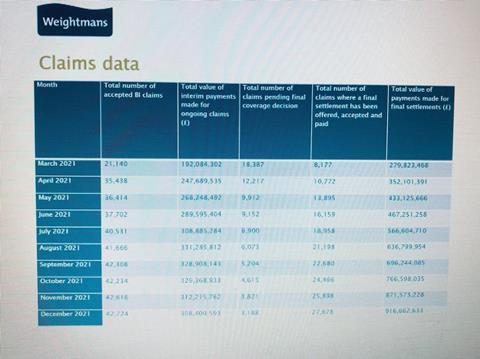

Despite policy wording and judgment interpretation challenges, insurers have made considerable progress through the BI claims backlog, added Weightmans solicitor Sarah Irwin, who talked webinar attendees through the FCA’s published stats.

As of 6 December 2021, 3,188 claims were pending a final coverage decision – Irwin described this as a big improvement compared to the 18,387 claims recorded in March 2021.

Although there was an immediate flurry of claims decisions following the Supreme Court judgment, Irwin noted a slowing down of progress between May and July last year.

For example, in April 2021, the total number of claims pending a final coverage decision amounted to 12,217 – down from 18,387 in March. This decreased further to 9,912 in May, however progress stalled in June 2021 as the number of pending claims only moved to 9,152.

Similarly, between July and August 2021, the total number of claims pending a final coverage decision only decreased slightly, in the grand scheme of things, from 6,900 to 6,073.

Irwin added that 35% of accepted claims are still waiting to receive a settlement.

She attributed this trend to a couple of factors, such as the immediate impact of the Supreme Court judgment waning as time has passed and the fact that more straightforward, easy to prepare cases were most likely dealt with first. This means that stalled progress could be down to discussions around more contentious claims.

This could include cases were the policy wordings were not directly included in the test case sample, so a bit of creative license is needed to apply the judgment learnings, or if policyholders are still experiencing Covid-related losses, meaning that indemnity periods are still being determined.

Irwin said: “The figures appear to show steady progress in the final settlement of claims throughout 2021 and in that loss adjusting process, but perhaps there has been a slow down in cover decisions being made and claims accepted.”

Outstanding issues

The litigation around BI claims is far from over, Irwin added, with a number of cases set to be heard this year.

These primarily focus around the outstanding issues that were not solved by the FCA’s legal proceedings – for example, aggregation, the treatment of government grants, clarifying the length of the cover period and the application of late payment damages.

She even described the case between pub chain company Stonegate Group and MS Amlin, which is due to go to trial in June 2022, as a “quasi test case” for the aggregation issue.

The claim, valued at £845m, considers Stonegate’s 791 pubs, restaurants and bars and whether its BI losses should come under one single claim or numerous independent claims with separate sub-limits.

Meanwhile, more confusion also reigns as a result of Lord Mance, who sat as the sole arbitrator in Certain Policyholders v China Taiping Insurance (UK) Co Ltd. According to Irwin, some of his decisions contradicted the original High Court judgment, published in September 2020 - for example determining that ‘vicinity’ did not just refer to a local, neighbourhood incident.

The discussion points raised by Weightmans flags one conclusion – that despite it being a year since the ‘clarity’ of the Supreme Court’s final ruling, we still have a long way to go before a solution to every conceivable BI predicament is created, if this is even possible.

Businesses – and especially SMEs – come in all shapes, sizes and models. I have a feeling a lot of the remaining work now is going to involve making coverage decisions on a claim-by-claim basis, considering the particular nuances of individual businesses. Although this may be more time consuming, hopefully it will lead to the right results.

No comments yet